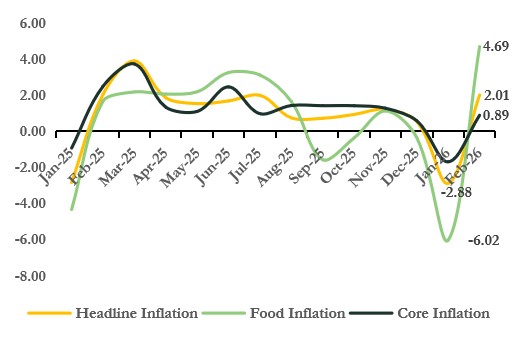

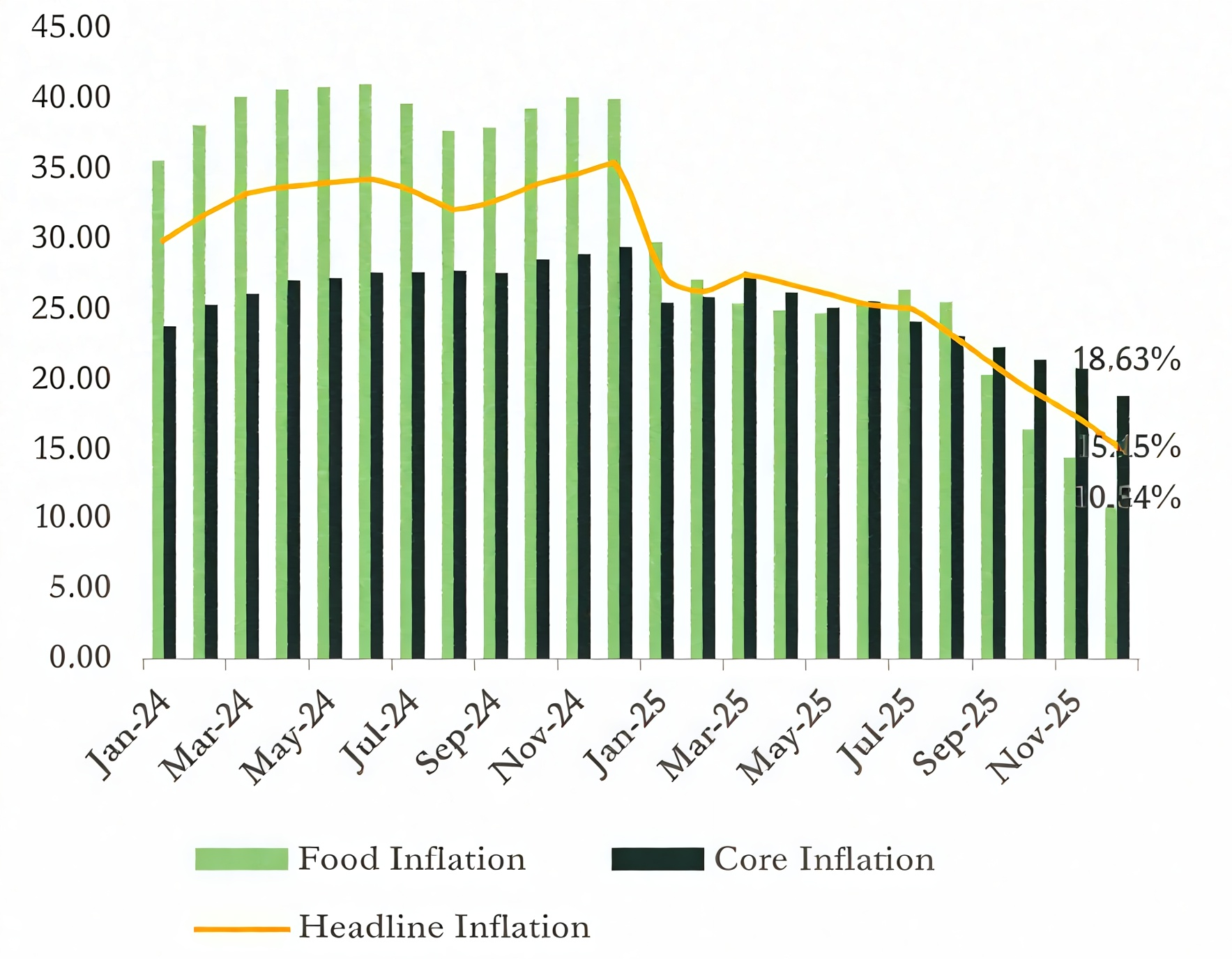

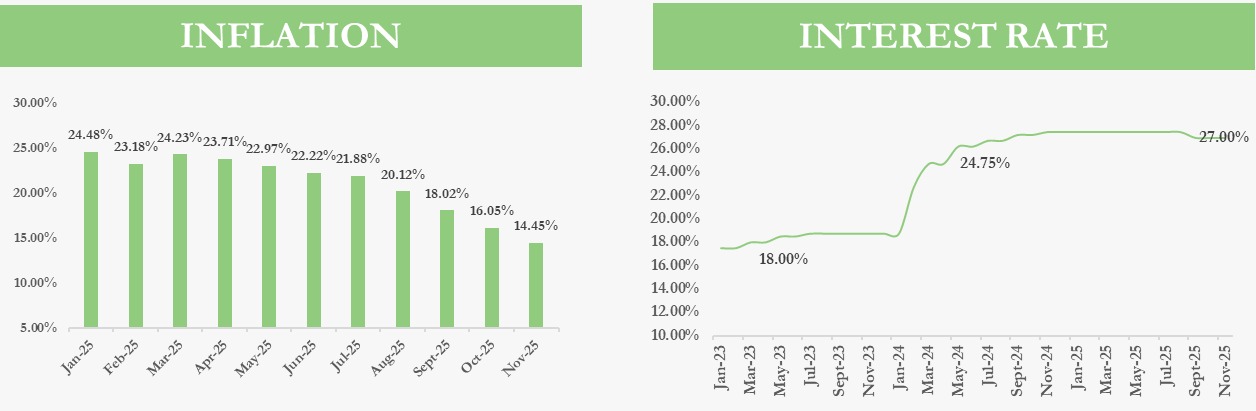

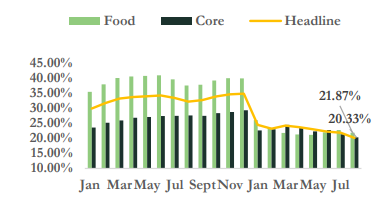

Headline Inflation Eases to 15.06% in February but Monthly Pressures builds.

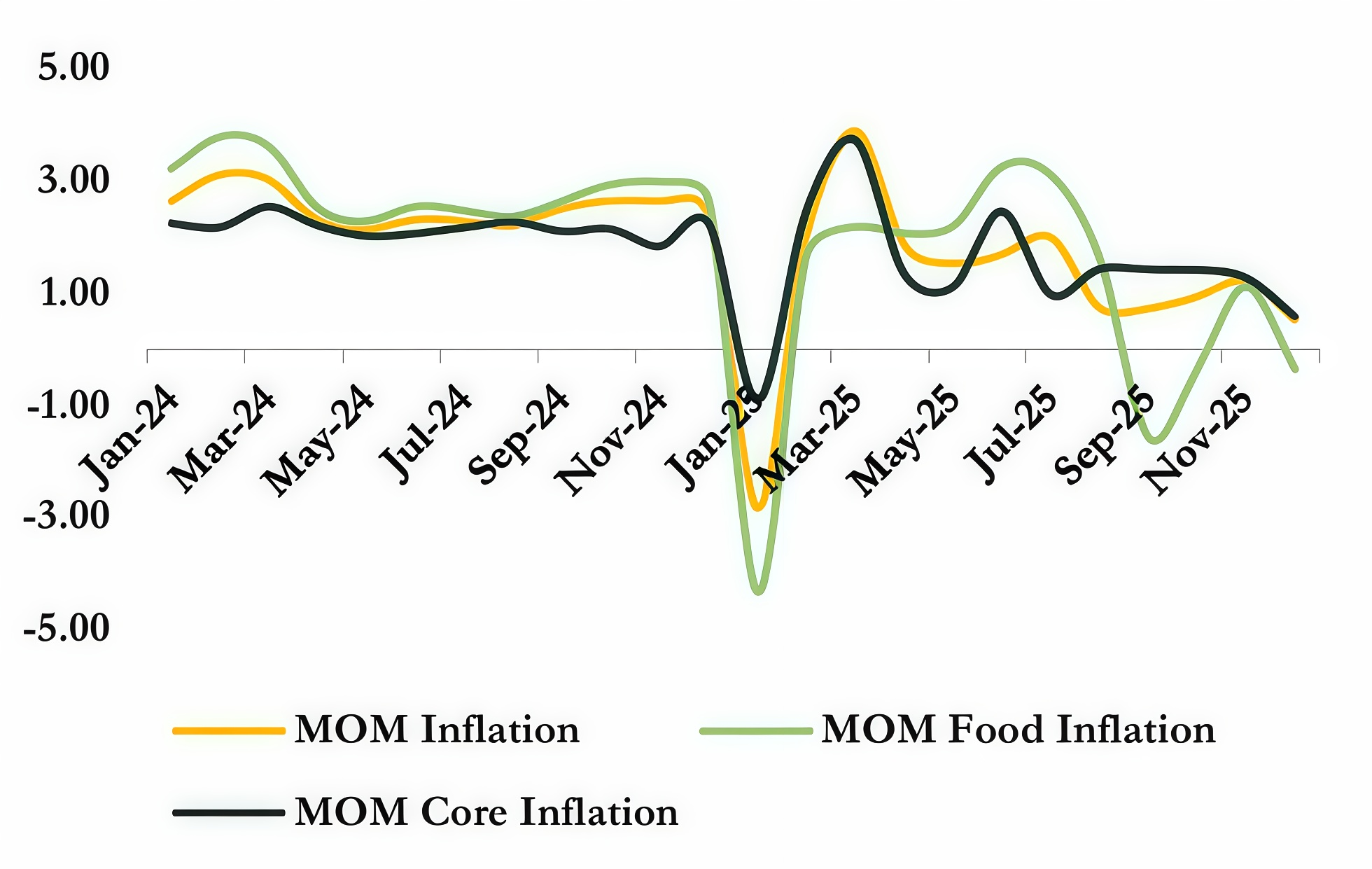

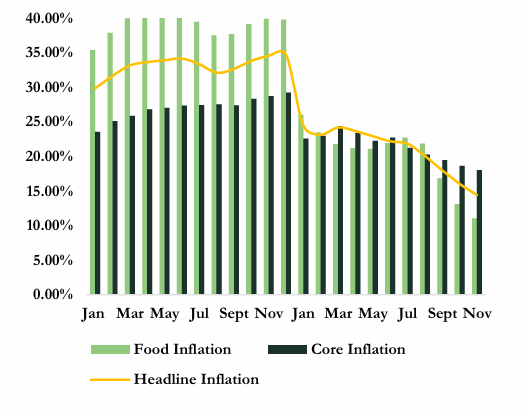

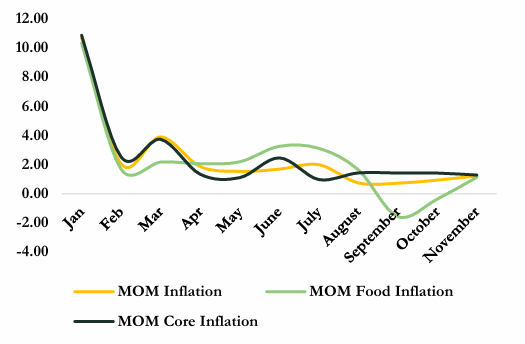

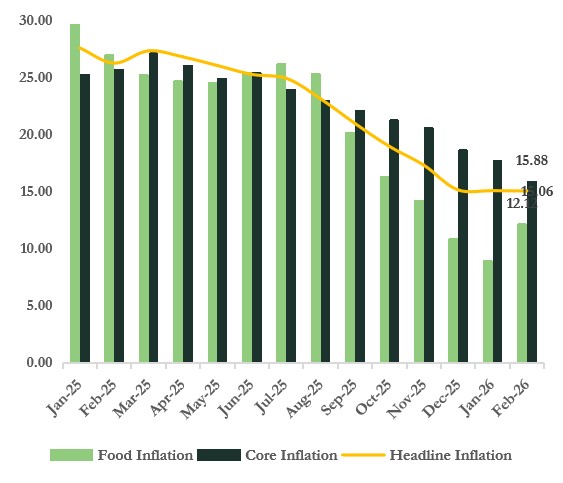

According to the National Bureau of Statistics, headline inflation in Nigeria eased marginally to 15.06% in February 2026 from 15.10% in January, marking an 11th consecutive month of disinflation. The moderation was driven by a decline in core inflation (15.88% from 17.72%), which offset the increase in food inflation (12.12% from 8.89%). On a month-on-month basis, headline inflation rose to 2.01% from -2.88%, indicating a short term rebound in price pressures

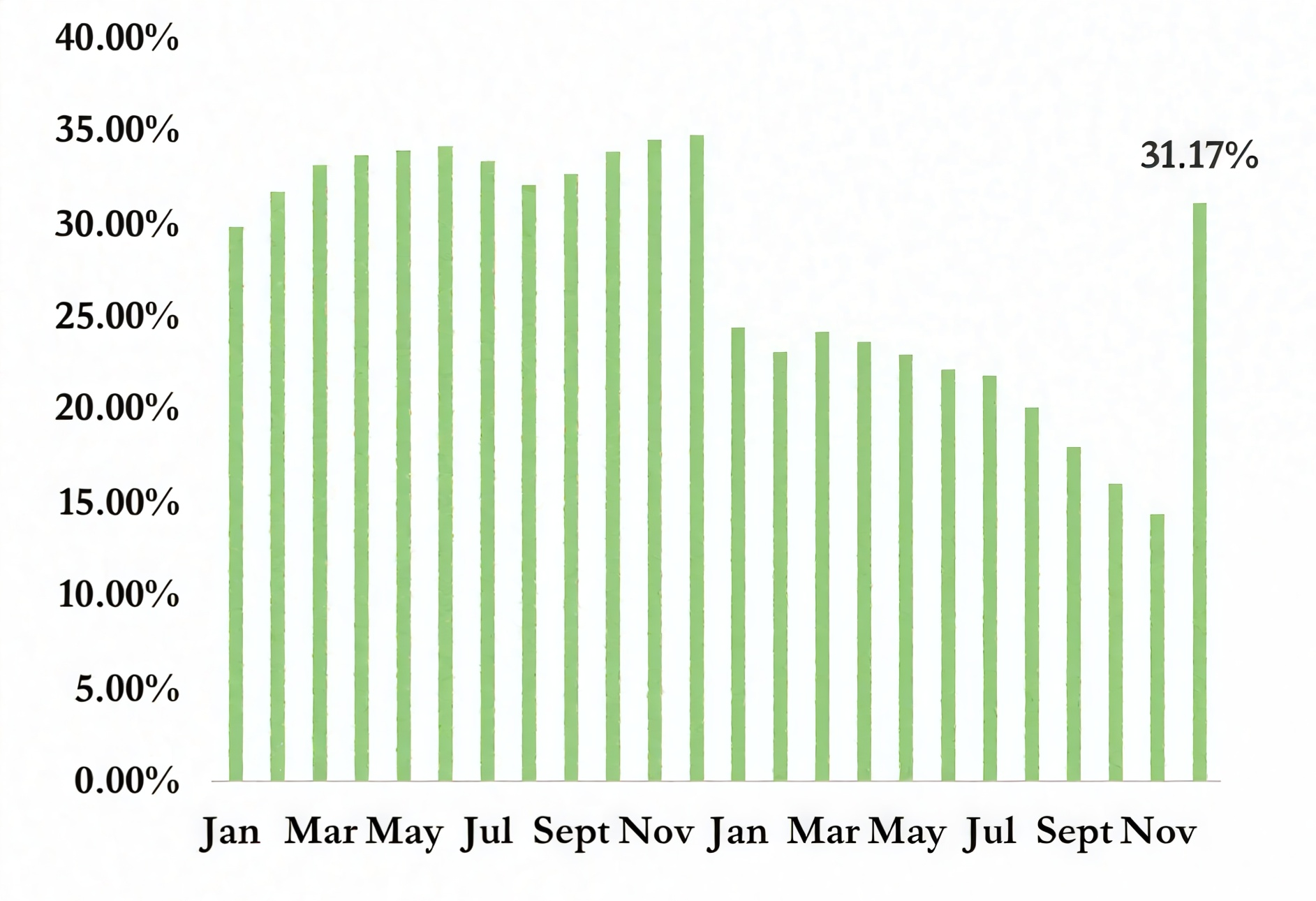

Disaggregated data shows that food inflation accelerated to 12.12% from 8.89% in January. Similarly, on a month–on– month basis, food inflation accelerated to (4.69% from a 6.02%) deflation recorded in January, the highest since rebasing, reflecting tightening food supply conditions as post-harvest gains fade and the farmers transition into the planting season. Additionally, persistent security and logistics constraints affect distribution to key consumption centers

Core inflation, which excludes volatile agricultural produce and energy, moderated to 15.88% vs 17.72% in January, but rose to (0.89% vs -1.69%), m-o-m, suggesting renewed underlying pressures. This uptick was driven by increases in the rent index (3.07% vs 0.72%) m-o-m, alongside a moderation in deflation within the transport (-0.26% vs -1.02%) m-o-m and restaurant components (1.12% vs -0.08%) m-o-m

OUTLOOK

Inflation is expected to edge higher in March 2026, potentially interrupting the recent disinflation trend. The disruption in the Strait of Hormuz amid tensions between the United States and Iran has elevated global oil prices, translating into higher domestic fuel costs (₦ 1250/per liter) and transportation expenses. In addition, the temporary depreciation of the naira is likely to increase imported inflation through exchange rate pass-through. Consequently, both food and core inflation are expected to rise modestly in the near term, with headline inflation likely to tick up slightly before stabilising, if energy and exchange rate pressures ease.

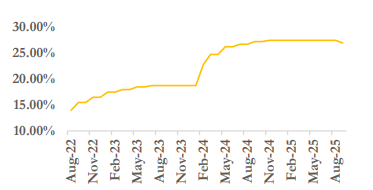

Y-o-Y Inflation Trend

M-O-M Inflation Trend