2025 Economic Review

Economic Growth Performance

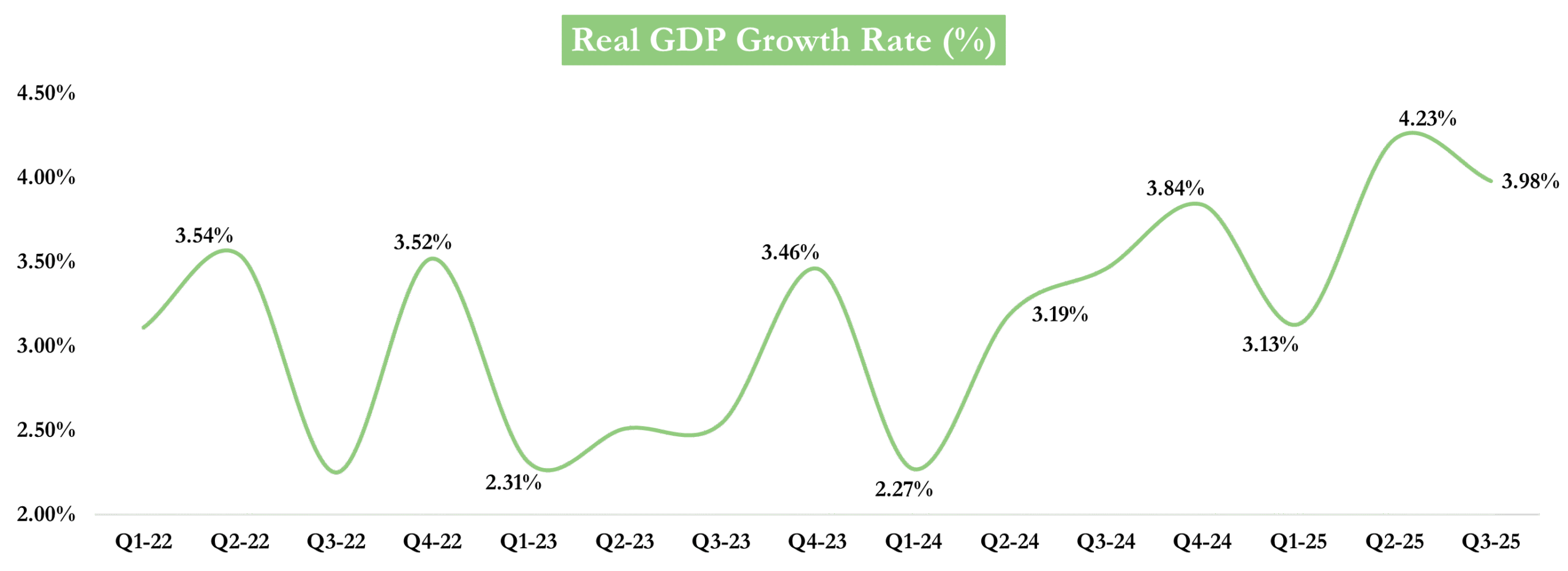

- Nigeria’s economy expanded by 3.98% y/y in Q3 2025, easing from 4.23% in Q2, its strongest growth since Q2 2021, but outperforming the 3.86% growth recorded in Q3 2024.

- The non-oil sector, which accounted for 96.6% of total output, grew by 3.91% vs Q2: 3.64%, supported by stronger activity in agriculture (3.79%), financial and insurance services (19.63%), trade (1.98%), construction (5.57%), and modest gains across ICT, real estate, and manufacturing.

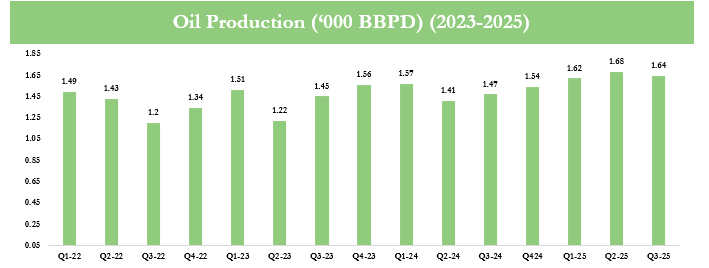

- In contrast, the oil sector grew by 5.84% y/y, a sharp slowdown from 20.46% in the previous quarter, reflecting weaker crude output. Oil production averaged 1.64 mbpd in Q3, slightly below Q2’s 1.68 mbpd but above the 1.47 mbpd recorded in Q3 2024.

Source: NBS, BRB Research

Inflation and Monetary Policy

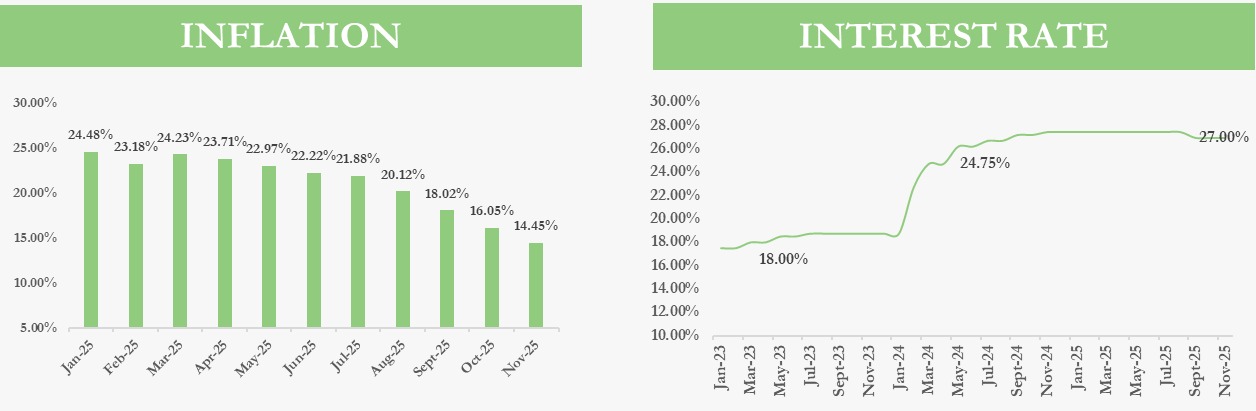

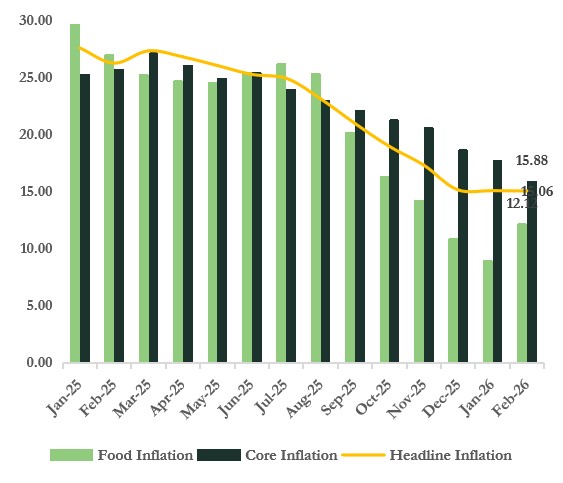

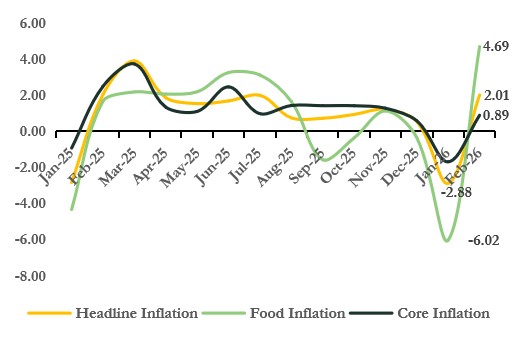

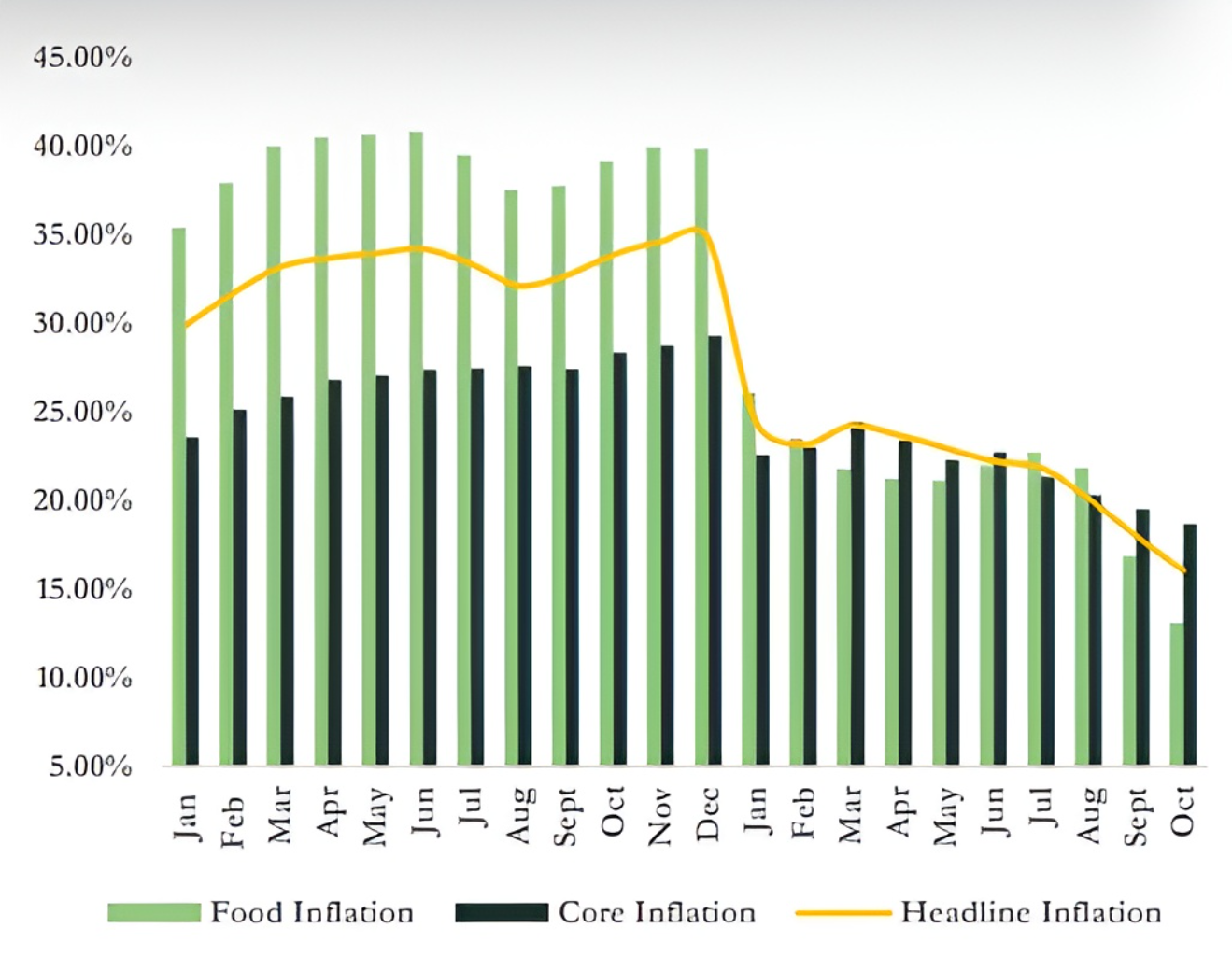

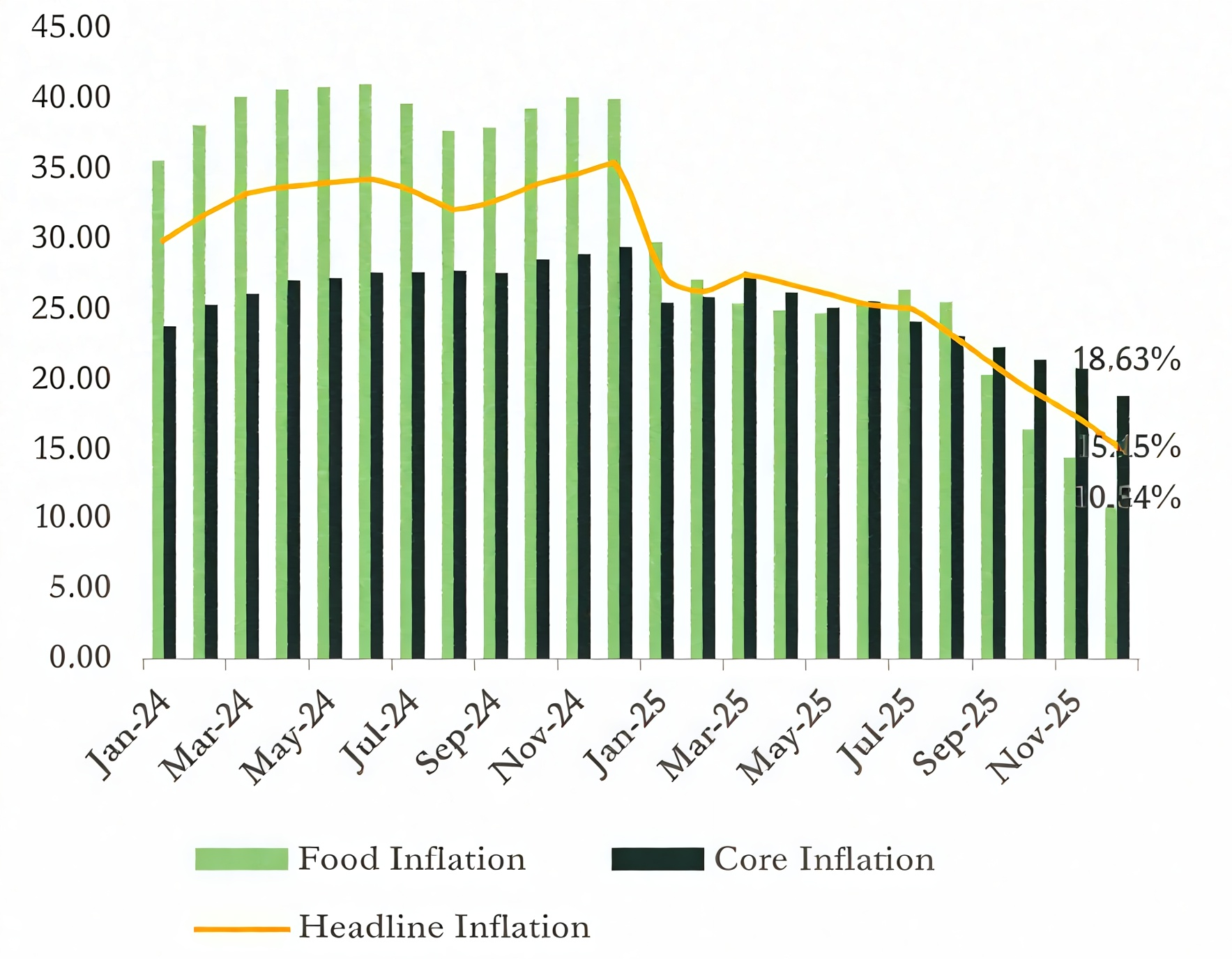

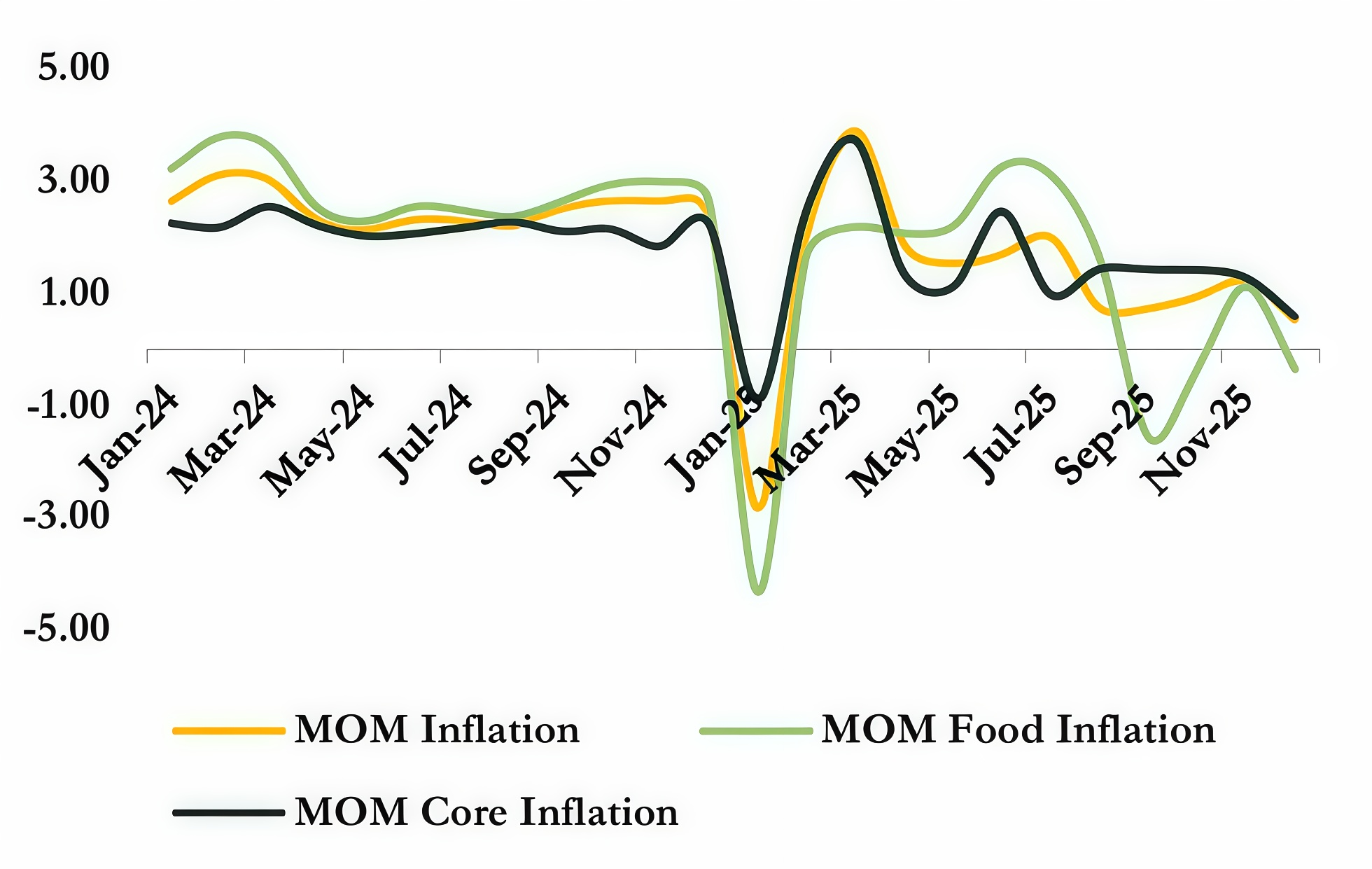

- Nigeria’s inflation environment has continued to improve, with headline inflation easing for the eighth consecutive month and settling at 14.45% from 16.05% year-on-year in November 2025. The deceleration has been driven largely by the rebasing effect, softer food price pressures, improved supply conditions, and a more stable foreign-exchange market. Core inflation remains elevated at 18.04% while Food inflation moderated to 11.08%, reflecting a gradual easing in underlying price pressures.

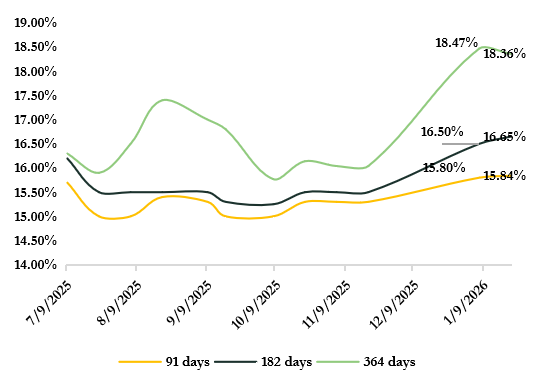

- Against this backdrop, the Central Bank of Nigeria maintained the MPR at 27% in November 2025, following a 50-bps reduction in September, as it sought to consolidate recent progress on disinflation. Although headline inflation continued to moderate, the MPC noted that underlying price pressures remain elevated, warranting a cautious pause. The adjustment of the policy corridor to +50/-450 bps from +250/-250 bps signals a subtly more accommodative liquidity framework. The stance shows a gradual shift from aggressive tightening toward a more balanced macro-stabilization

Source: NBS, BRB Research Source: Investing.com, BRB Research

Exchange Rate and Foreign Reserves

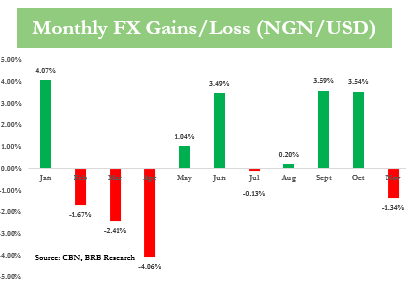

- Nigeria’s foreign exchange market stabilized in 2025 following previous periods of sharp depreciation, supported by CBN initiatives including the Electronic FX Matching System (EFEMS), transparent auction processes, and partial market liberalization. These measures enhanced liquidity and narrowed the gap between official and parallel market rates, with the naira strengthening to ₦1,446 per US dollar by November 2025 from ₦1,535 per US dollar at the end of 2024.

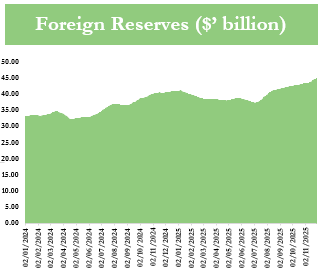

- Foreign reserves rose from USD 40.2 billion at the end of 2024 to USD 44.67 billion by November 2025, reflecting strengthened external sector conditions. The recent Eurobond issuance of $2.35 billion provided a significant boost to reserve buffers, complementing gains from improved oil production, firmer export receipts, steady remittance inflows, and renewed foreign portfolio investment.

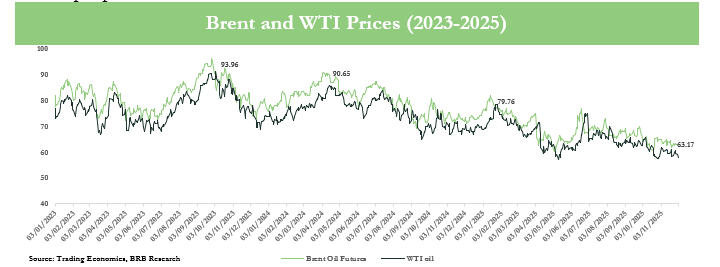

Oil Market

- The 2025 oil market began the year in relative balance, with temporary supply disruptions from seasonal factors and unplanned non-OPEC+ outages offset by robust structural supply. Demand growth remained moderate amid macroeconomic uncertainty, resulting in stable prices with limited volatility.

- In Q2, OPEC+ began rolling back voluntary production cuts while output from the U.S. and Brazil remained strong, leading to rising supply that outpaced demand and triggered bearish sentiment. By Q3, oversupply became the defining feature, as global production exceeded demand, inventories accumulated, and analysts revised downward full-year price expectations.

- The year closed with the supply glut persisting into Q4; inventories remained elevated, and prices stabilized below mid-year peaks following OPEC+ guidance on potential early-2026 output pauses.

Oil Production

- In Q3 2025, Nigeria’s average daily oil production stood at 1.64 million barrels, up 0.17 mbpd from Q3 2024 but slightly below Q2 2025’s 1.68 mbpd. The sector’s gradual recovery in 2025 was supported by improved security, enhanced pipeline integrity, and more coordinated upstream operations. Production averaged 1.66 mbpd in H1, peaked at 1.68 mbpd in Q2, the highest since 2020, and moderated slightly in Q3, reflecting ongoing operational adjustments and maintenance activities.

- The rebound helped reinforce external balances and foreign-exchange supply, but output volatility remained a feature of the sector’s performance. Despite the improvement, production levels fell short of the government’s 2025 target of 2.06 million barrels per day, reflecting ongoing structural challenges. Crude theft, infrastructure constraints, and intermittent operational disruptions continued to weigh on capacity utilization, limiting the pace of recovery.

Source: NBS, BRB Research

Economic Outlook for year 2026

2026 Outlook

- Nigeria’s economy is expected to expand over the near term, with the IMF projecting GDP growth of 3.9% in 2025 and 4.2% in 2026, supported by stable oil inflows, improving oil production levels, and greater policy consistency.

- Headline inflation is expected to continue its moderating trend in 2026, easing toward 11.56% by year-end, supported by a stable exchange rate, cautious monetary policy, and weaker energy prices. This disinflationary environment is likely to provide the Central Bank of Nigeria with scope to maintain a neutral to mildly accommodative monetary policy stance. We anticipate a potential recalibration of the MPR, with a projected easing of around 200 basis points by mid-2026, contingent on inflation remaining firmly anchored and underlying price pressures remaining subdued.

- Several risks could reverse the projected downward trend in inflation in 2026. Pressure on the exchange rate may increase the cost of imported goods, while elevated government spending ahead of elections could inject additional liquidity, boosting prices. Structural challenges, including insecurity in key food-producing regions, may constrain supply and exert upward pressure on food prices. External shocks, such as volatility in global oil markets, also represent a potential upside risk to inflation during the year.

- Despite these challenges, higher foreign reserve buffers and reforms in the foreign-exchange market, including enhanced transparency and more efficient EFEMS operations, should help limit exchange-rate volatility and strengthen overall broader macroeconomic stability. These developments, alongside easing inflation and relatively stable macro fundamentals, are likely to support investor sentiment and attract modest portfolio inflows over the course of the year.

- The macroeconomic environment nonetheless remains sensitive to external and domestic shocks. Oil-price volatility continues to pose the most significant risk to fiscal stability and FX supply, while uncertainty around the revised Capital Gains Tax framework and lingering security concerns may temper investor appetite in the near term. Even so, the broader environment suggests cautiously improving conditions for Nigeria’s asset management and investment industry in 2026.

- Global oil market dynamics will be pivotal for Nigeria in 2026, with a structural supply surplus expected to persist due to strong non-OPEC+ production from the U.S. and Brazil and a measured supply approach from OPEC+. Demand growth will remain concentrated in non-OECD Asia, while elevated inventories are likely to keep Brent crude in the mid-to-low $50s per barrel. A potential peace deal between Russia and Ukraine could further soften prices if sanctions on Russian oil are eased, adding additional barrels to the market. Although geopolitical disruptions could still trigger short-term volatility, sustained low prices may eventually dampen non-OPEC+ investment.

Equities Market Review

Nigeria Equities Market Performance 2025

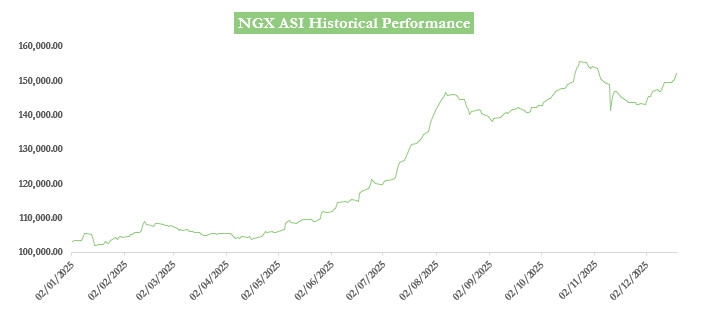

The Nigerian equity market delivered a powerful yet volatile performance in 2025, emerging as one of the strongest markets globally. For most of the year, sentiment was supported by market-friendly reforms, resilient corporate earnings, improved foreign-exchange conditions and strong domestic liquidity.

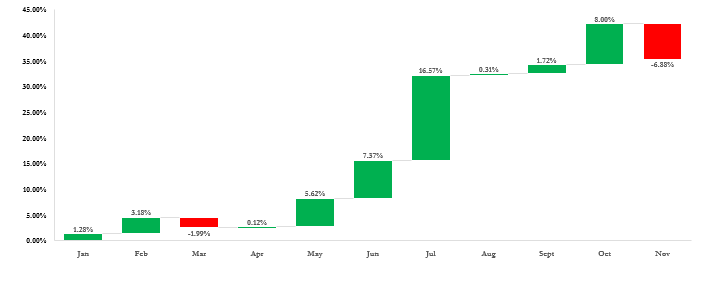

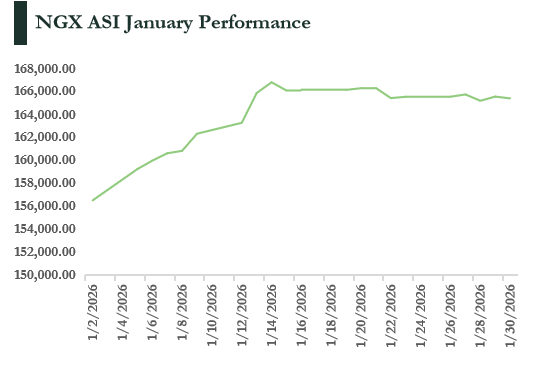

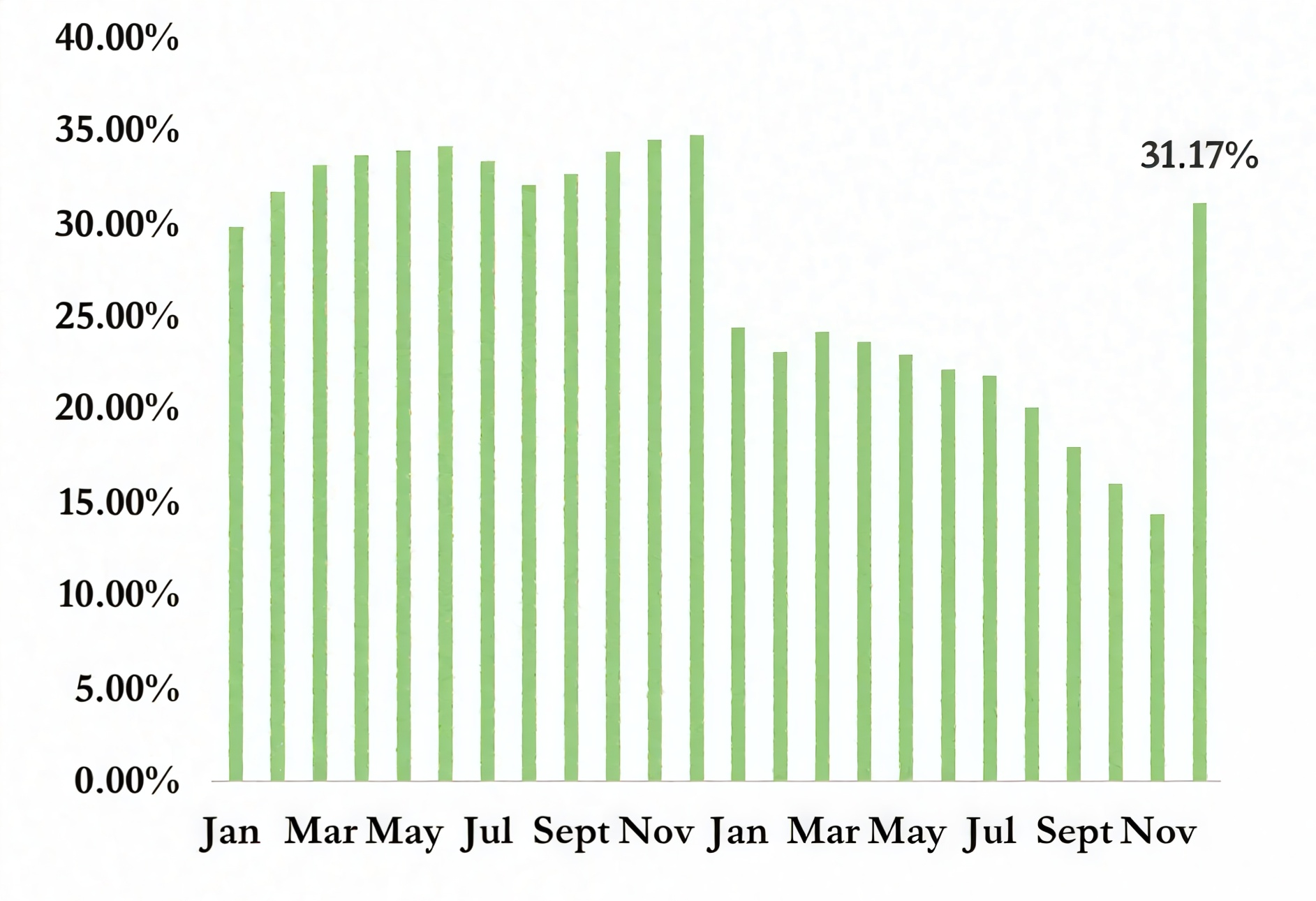

Market capitalization rose from ₦62.76 trillion at end-2024 to ₦91.29 trillion by late November, reflecting a 45.45% increase in investor wealth. Gains strengthened through the third quarter, with the ASI up 16.57% by mid-year and nearly 50% by October. The NGX All-Share Index (ASI) also advanced significantly, climbing from 102,926.40 points to over 150,000 points in October before moderating to 143,520.52 in November.

Investor participation was robust, driven by both domestic and foreign flows. Total transactions for the first eight months of the year rose by 99% to ₦6.92 trillion. Foreign portfolio inflows increased by 122% to ₦1.45 trillion, aided by improved FX liquidity and clearer exit conditions, whereas domestic investors contributed over ₦5.46 trillion, reinforcing their leadership in market activity. These flows were complemented by the performance of several high-growth stocks, with tickers like BetaGlass, MTN, Ellah Lakes, WEMA Bank, NCR, MBENEFIT, UACN, and ASO Savings delivering returns ranging between 100% and more than 500%, reflecting strong liquidity and high conviction in select counters.

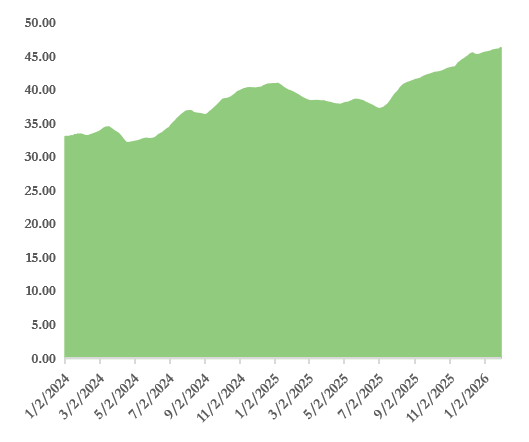

NGX ASI Monthly Returns

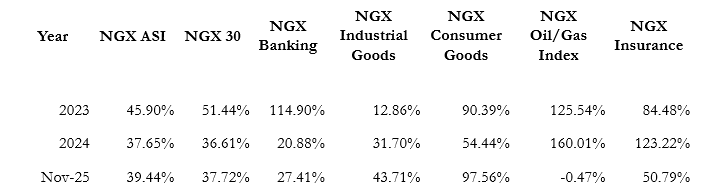

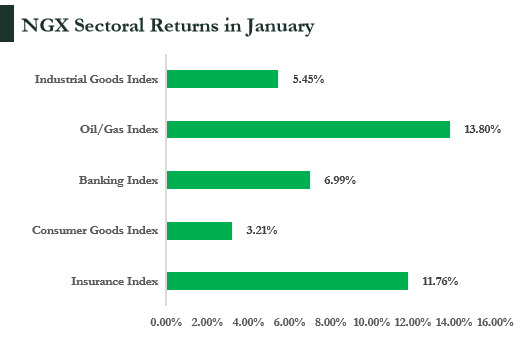

Sector performance highlighted the breadth of the rally. Consumer goods companies led with over 100% year-to-date gains by October, supported by strong local production and pricing resilience amid FX constraints. The Insurance Index rose sharply on recapitalization expectations, while the Banking Index, though third in returns, remained the most actively traded, reflecting strong institutional interest. Industrial goods stocks also saw significant demand, whereas the Oil & Gas Index lagged for most of the year due to sector-specific challenges.

NGX Sectoral Performance (2023-2025)

However, the positive momentum was interrupted in November by the sharpest correction of the year. Market capitalization fell by about ₦6.54 trillion following uncertainty over the proposed changes to the Capital Gains Tax framework. The shift from a flat 10% rate to a progressive structure of up to 30% triggered aggressive profit-taking and capital repatriation by foreign investors. Combined with geopolitical concerns, the policy announcement dampened sentiment and illustrated how quickly fiscal decisions can offset months of progress driven by monetary reforms and FX stability.

2026 Outlook

Outlook

Building on a robust 2025, Nigeria’s equities market is poised for a strong 2026 performance, with potential total returns exceeding 30%, supported by ongoing reforms, macroeconomic stability, and stronger corporate earnings. Key growth drivers include continued sectoral diversification, with consumer goods, industrials, and financials expected to anchor performance, alongside rising dividends that enhance total shareholder returns.

Market sentiment will be increasingly shaped by company-specific fundamentals, with investors focusing on earnings quality, balance sheet strength, and cash-flow resilience. The anticipated listing of NNPC Limited and Dangote Refinery next year could serve as a major liquidity and valuation catalyst, attracting both domestic and foreign capital.

Further support is expected from positive macroeconomic factors, including easing inflation, stable interest rates, and an improved foreign-exchange environment, as well as regulatory clarity that strengthens investor confidence. Active portfolio management, diversification across high-quality sectors, and close monitoring of earnings, FX developments, and policy changes will remain essential to navigate potential volatility and capture upside opportunities.

With the economic drivers such as sectarial diversification, industrial consolidation and real financial inclusion properly deployed will improve the economic temperature of the nation