Nigeria's Financial Glow-Up: Off the Naughty List and into the Big Leagues

A Quick Look at the Big Picture

Picture this: on 24 October 2025, Nigeria got some brilliant news. The world’s top financial watchdog, the Financial Action Task Force (FATF), officially took the country off its list of “Jurisdictions under Increased Monitoring”—which everyone really just calls the “grey list”. Think of it as being let out of the financial sin bin. This wasn’t just a pat on the back; it was the result of a tough, two-year reform marathon that’s set to shake up Africa’s biggest economy in the best way possible. Getting off this list is a huge strategic win. It tells the world that Nigeria is a safer bet, boosting its street cred in global finance and opening the taps for fresh investment and growth. This report takes a deep dive into what this all means for Nigeria’s money market—the engine room of its financial system. We’ll look at the hard graft that went into the reforms, what the market looked like before, and how this news is changing the game for everyone involved.

The main takeaway? Getting the all-clear from the FATF is like a shot of adrenaline for the Nigerian money market. For starters, it’s a massive confidence boost for international investors. We expect to see more foreign cash flowing into short-term government and corporate IOUs, like Treasury Bills (T-Bills) and Commercial Papers (CPs). This means more cash in the system, which is always a good thing. Secondly, with Nigeria looking less risky, the cost of borrowing should drop. That’s great news for the Government, which can save money on its debts, and for top-tier companies, who will find it cheaper to raise funds. It might finally stop the Government’s borrowing from “crowding out” everyone else. For the players on the ground, the perks are real.

The Central Bank of Nigeria (CBN) gets a gold star for its policies. Commercial banks will find it easier and cheaper to deal with their international partners, with less red tape to cut through. And for the finance chiefs at big companies, a livelier CP market means an easier way to manage their day-to-day cash flow. But let’s not get ahead of ourselves. While the outlook is sunny, it comes with a condition. The FATF is keeping a close eye on Nigeria for the next 12 months to make sure these changes stick. So, all the long-term benefits we’re talking about depend on the country staying on the straight and narrow. This isn’t the finish line; it’s the start of a new era where keeping up these high standards is the key to Nigeria’s financial health and prosperity.

The FATF Lists: A Global Report Card for Finance

To really get why this is such a big deal for Nigeria, you need to understand what the FATF is and why its lists matter so much. Set up by the G7 in 1989, the FATF is basically the global referee for keeping money clean. It sets the international rules for fighting money laundering, terrorist financing, and the funding of nasty weapons. The rulebook is known as the 40 Recommendations, and countries are expected to follow it. The FATF checks up on them with peer reviews, called Mutual Evaluations, to see if they’re just talking the talk or actually walking the walk.

The "Grey" and "Black" Lists Explained

Based on these check-ups, the FATF publicly names and shames countries with dodgy financial systems in two lists, which get updated three times a year. The difference is important:

- The Black List (High-Risk Jurisdictions subject to a Call for Action): This is for countries with really serious problems that aren’t playing ball. The FATF tells its members to be extra careful with them and can even call for financial sanctions. It’s the worst place to be and can leave a country financially isolated.

- The Grey List (Jurisdictions under Increased Monitoring): This is for countries that have some weaknesses but have promised to fix them with a clear action plan. They’re watched closely and have to show they’re making progress. It’s not as bad as the black list, but it’s still a big red flag for the rest of the world, signalling higher risk and causing a whole host of economic headaches. This is the list Nigeria was on—a country trying to do the right thing.

The Price of Being on the Grey List

Being on the grey list isn’t just bad for your reputation; it’s bad for your wallet. It acts like a massive barrier to investment and trade. Global banks and investors, wanting to stay out of trouble themselves, tend to back away from grey-listed countries.

Here’s how it works: when a country is on the grey list, international banks have to do “Enhanced Due Diligence” (EDD) on any transaction linked to it. EDD is a pain—it’s expensive, takes ages, and involves a lot more paperwork. To avoid the hassle, many banks just “de-risk” by limiting or cutting ties with banks in that country altogether. This has a real, measurable impact. A major 2021 study by the International Monetary Fund (IMF) found that being on the grey list cuts a country’s capital inflows by an average of 7.6% of iits GDP. That includes a 3.0% drop in foreign direct investment and a 2.9% drop in portfolio investment.

For a country like Nigeria, which relies on international trade, money sent home from abroad, and investment, this really stings. It means less cash in the system, higher costs for moving money, and fewer interested investors. This context shows just how massive a victory getting off the list truly is.

Nigeria's Two-Year Financial Makeover

Nigeria’s journey from the grey list to the all-clear was a focused, two-year national effort, driven by top-level political will and some deep, structural spring-cleaning. The whole saga kicked off in February 2023 when the FATF put Nigeria on its watch list, and it all came to a happy conclusion in October 2025.

A Wake-Up Call in 2023

When Nigeria landed on the grey list, the FATF pointed out several weak spots in its defences against financial crime. The message was loud and clear: Nigeria had to get tougher on enforcement, get its various agencies to work together better, and make its financial system more transparent. Instead of sulking, the Nigerian government saw it as a “call to action”—a golden opportunity to fast-track reforms that were long overdue and central to its economic transformation plans.

The Action Plan and the Big Fixes

In response, Nigeria signed up to a hefty 19-point action plan to tackle every single issue the FATF had raised. Putting this plan into action was a massive undertaking, involving big changes to laws, institutions, and day-to-day operations.

- Putting Muscle into the Law: The bedrock of the reform was getting two key laws up and running properly: the Money Laundering (Prevention and Prohibition) Act, 2022, and the Terrorism (Prevention and Prohibition) Act, 2022. These laws gave the authorities the teeth they needed to supervise, enforce, and prosecute financial crimes, bringing Nigeria’s rulebook in line with global standards.

- Getting Everyone on the Same Page: A huge part of the success was creating a central command for the effort. The Nigerian Financial Intelligence Unit (NFIU), led by its Director/CEO, Ms Hafsat Abubakar Bakari, was the star player. The NFIU led a National Task Force that brought everyone to the table—the Central Bank, the Ministry of Finance, the Ministry of Justice, the Economic and Financial Crimes Commission (EFCC), and even folks from the private sector. This “all-hands-on-deck” approach made sure the reforms happened smoothly, without the usual squabbling between agencies.

- Shining a Light with the Beneficial Ownership Register: One of the big criticisms in Nigeria’s 2021 FATF review was that it was too easy to hide who really owned a company. A major win was the launch of a public Beneficial Ownership Register, which made it much clearer who was pulling the strings behind Nigerian companies.

- Tougher Supervision and Enforcement: The reforms also meant stricter, more risk-focused supervision of banks and what are known as Designated Non-Financial Businesses and Professions (DNFBPs)—think estate agents, lawyers, and casinos, which can be hotspots for dodgy dealings. This was backed up by practical steps, like training law enforcement on how to gather evidence, improving the quality of suspicious. transaction reports, and showing a real increase in the number of complex money laundering cases being investigated and prosecuted.

The Results Are In

The hard work paid off. Nigeria ticked off all 19 items on its action plan ahead of schedule. This progress was officially recognised with upgrades to its compliance ratings on several key FATF Recommendations. Specifically, Nigeria’s scores for Recommendations 23, 24, 25, 28, and 32 all went from “Partially Compliant” to “Largely Compliant” or “Compliant”.

After a successful on-site visit from an FATF team to check that the reforms were real and would last, the FATF Plenary gave Nigeria the green light on 24 October 2025. President Bola Ahmed Tinubu celebrated the news as “a major milestone in Nigeria’s journey towards economic reform, institutional integrity and global credibility” and a “strategic victory for our economy”. While the official news is clear, some mistaken reports have circulated suggesting Nigeria is still on the list, showing that perceptions can take a while to catch up. This just goes to show how important it is for Nigeria to keep shouting about its commitment to these reforms to win over any remaining doubters.

The Nigerian Money Market: A User's Guide

The Nigerian money market is the bedrock of the country’s financial system. It’s the main stage for short-term borrowing and lending, a bit like a financial flea market for IOUs that are due within a year. It’s vital for keeping the government and banks topped up with cash, helping the central bank’s policies ripple through the economy, and giving people a safe place to park their spare funds. To give you an idea of its size, as of August 2025, money market funds in Nigeria were managing a cool ₦3.59 trillion.

The Main Players and What They Do

The market is a bustling place, with a few key players calling the shots:

- Central Bank of Nigeria (CBN): The CBN is the top dog, the ultimate regulator. It sets the main interest rate (the Monetary Policy Rate, or MPR), controls the amount of cash sloshing around the system through its Open Market Operations (OMO), and issues the Government’s short-term IOUs.

- Debt Management Office (DMO): This is the government agency in charge of the national debt. It teams up with the CBN to decide when and how many government securities, like T-Bills, to sell.

- Commercial Banks: As the main go-betweens, banks are the most active players. They lend to each other to manage their daily cash needs and are huge investors in government securities like T-Bills.

- Non-Bank Financial Institutions (NBFIs) and Companies: This is a mixed bunch, including pension funds, asset managers, insurance firms, and big companies. They jump in as investors looking for a safe, quick return, and in the case of companies, they also issue their own IOUs (Commercial Papers) to raise cash for things like stock and wages.

The Hottest Products on the Shelf

While there are a few different instruments, two really dominate the market:

- Nigerian Treasury Bills (T-Bills): These are short-term IOUs issued by the Nigerian Government via the CBN. You buy them for less than their face value and get the full amount back when they mature. They come in 91-day, 182-day, and 364-day flavours and are seen as the safest bet in town because they’re backed by the full might of the government.

- Commercial Papers (CPs): These are unsecured, short-term IOUs from big, reputable companies. CPs are a flexible and often cheaper way for firms to get cash for short-term needs than going to a bank. In Nigeria, they can be issued for up to 270 days and are traded on exchanges like the FMDQ.

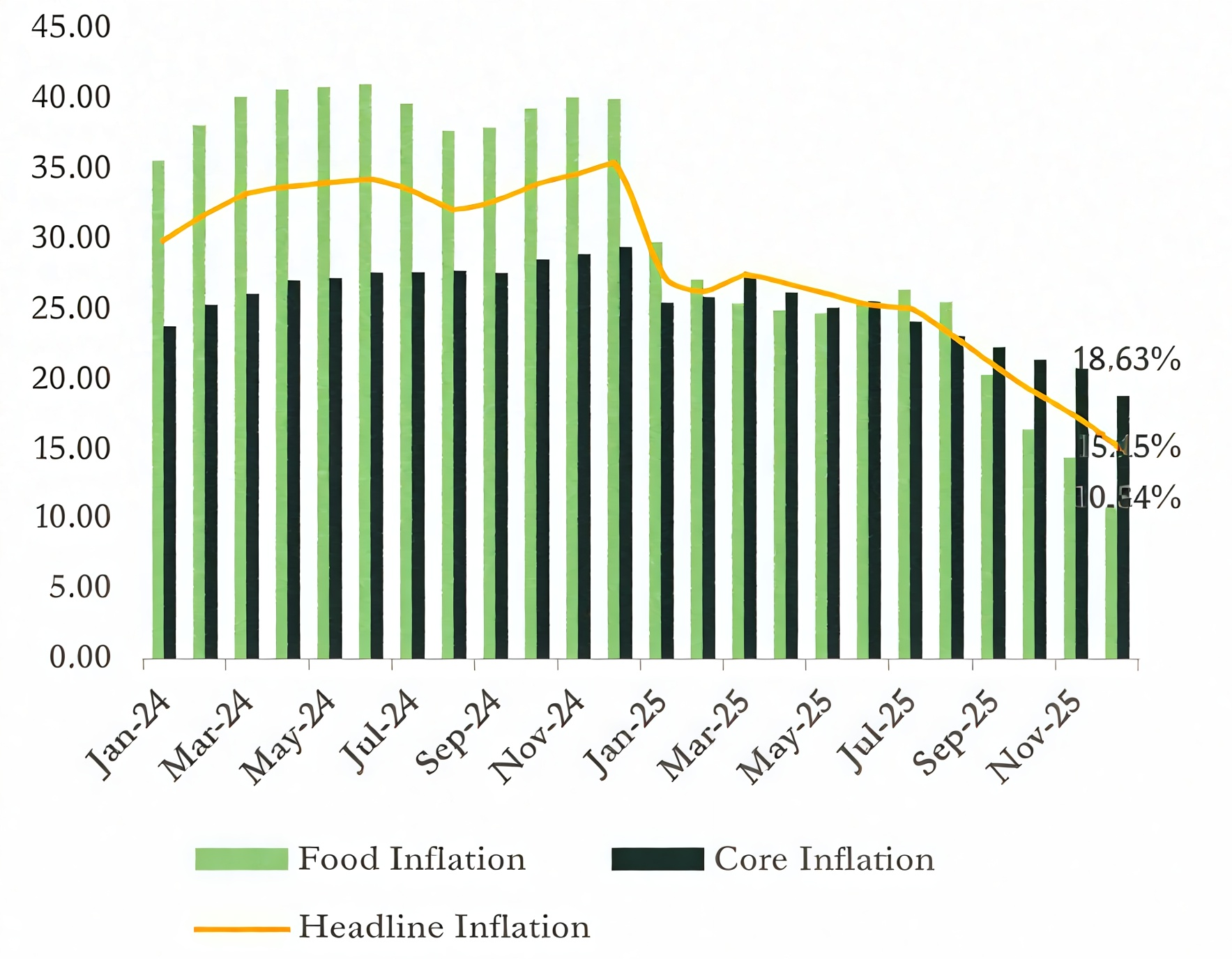

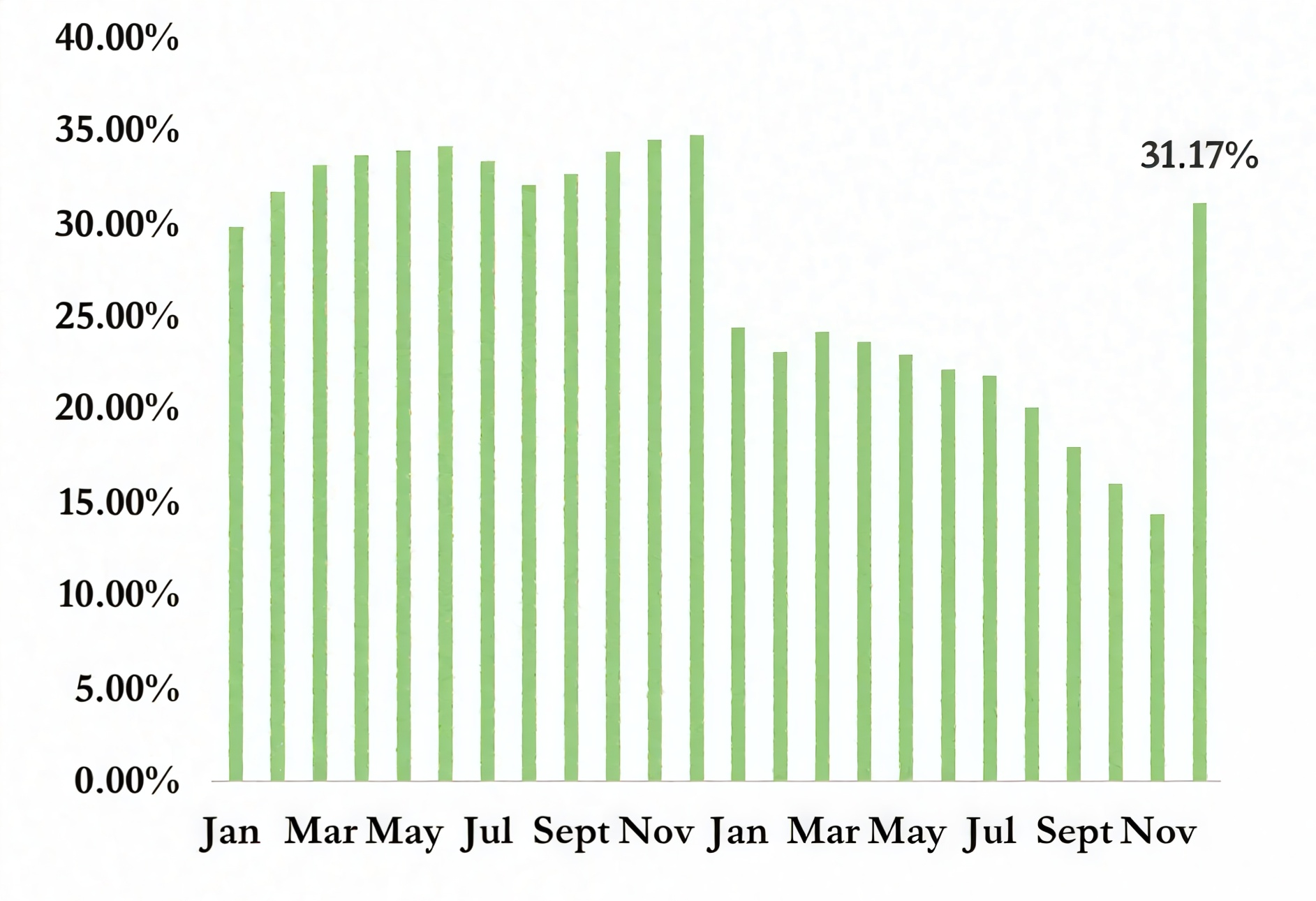

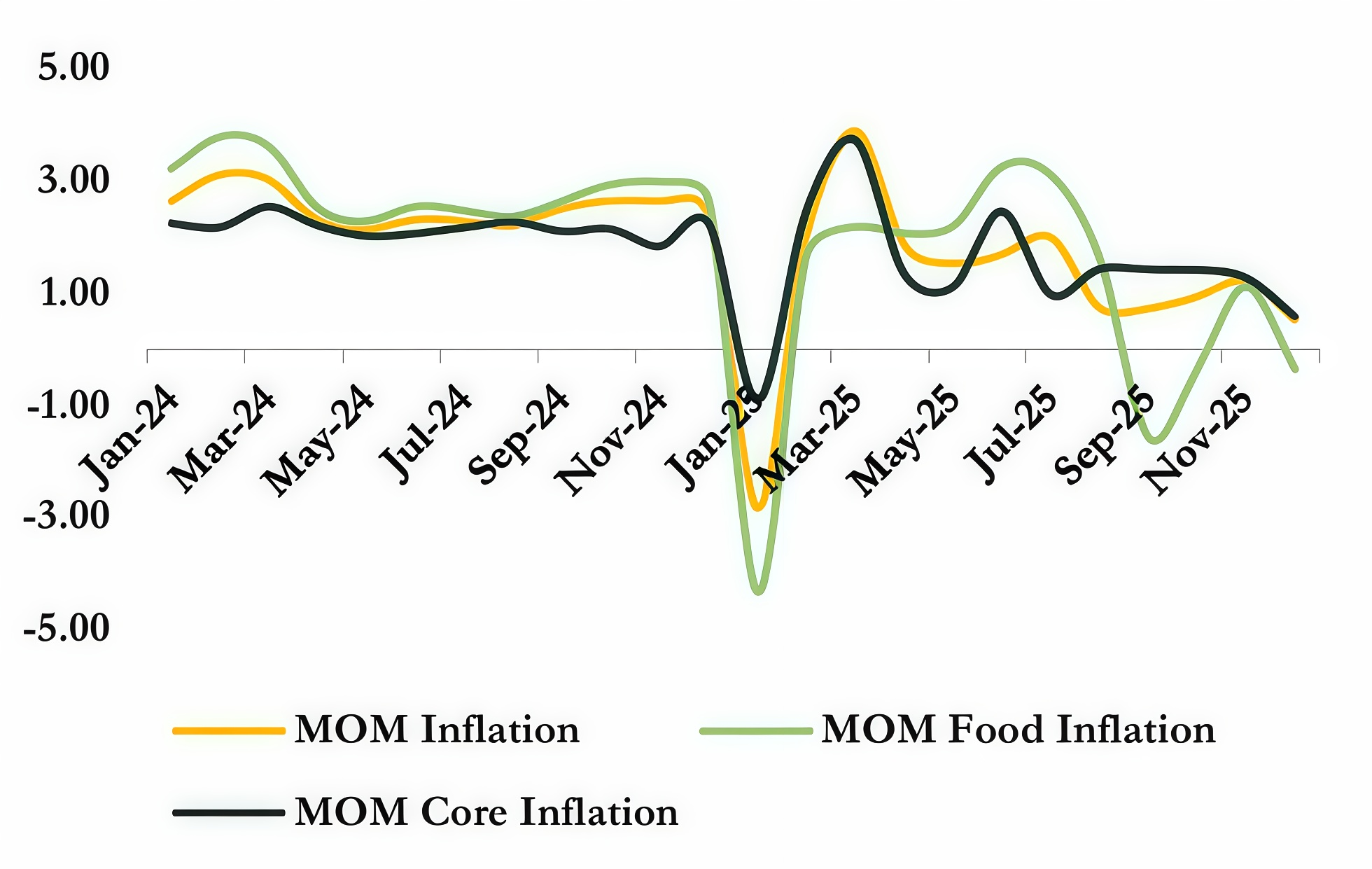

The Economic Weather Report (Late 2024 - Early 2025)

The FATF news didn’t happen in a vacuum. Nigeria’s economy was going through a challenging but exciting phase. Here’s the backdrop:

-

Interest Rates on the Rise: To fight off stubborn inflation, the CBN had been on a mission, hiking the MPR by a massive 875 basis points to a record 27.50% by November 2024.

-

Pesky Inflation: Although it was starting to cool down, inflation was still high, eating into people’s spending power and keeping the pressure on the CBN.

-

A Shake-Up in Foreign Exchange: The government had made some big moves, like floating the naira and clearing a huge backlog of foreign exchange debts. This caused the currency’s value to drop sharply but was aimed at creating a fairer, more transparent system.

This mix of high interest rates and the Government’s need to borrow a lot of money created a specific squeeze in the money market. The juicy yields on risk-free T-Bills made them irresistible to local investors. This led to a “crowding-out” effect, where the Government’s borrowing hoovered up most of the available cash, making it harder and pricier for private companies to raise money by issuing CPs. It’s against this backdrop of tight cash and high government borrowing costs that the FATF’s decision lands with such a splash.

What This All Means for the Money Market

Getting Nigeria off the FATF grey list is a game-changer for the country’s money market. The effects are wide-ranging, touching everything from the amount of cash in the system to the price of investments and the way everyone does business. It has the power to kick-start a positive cycle, undoing many of the pressures the market has been under.

More Cash, More Investment

The most immediate and obvious effect is the surge in confidence among international investors. This move is a powerful, independent stamp of approval on Nigeria’s reforms, basically telling the world that the country is “open, compliant, and ready for deeper financial integration”. This renewed faith is expected to bring in a flood of foreign money, reversing the capital flight we saw when Nigeria was on the list. This new cash will mainly flow into the money market through Foreign Portfolio Investment (FPI) in easy-to-trade, short-term instruments like T-Bills and top-quality CPs. The IMF’s research suggests that being on the grey list can slash capital inflows by as much as 7.6% of GDP, which means the potential for a bounce-back is huge. This wave of foreign currency won’t just boost the amount of money available for lending; it will also shore up Nigeria’s foreign exchange reserves and help stabilise the naira. The extra liquidity will ease the squeeze caused by the CBN’s high interest rates, making life easier for both borrowers and lenders.

A Fresh Look at Risk and Rewards

A huge impact of the delisting is the rethink of Nigeria’s country risk premium. The FATF grey list is a global risk marker; taking it away lowers the perceived danger of investing in Nigeria. Financial experts are widely predicting that this will lead to a drop in the extra return (the risk premium) that international investors demand for holding Nigerian assets. This repricing of risk will directly affect the yields on money market instruments:

-

Treasury Bills: With more foreign buyers and a lower risk premium, the yields on T-Bills are set to fall. This will directly cut the Government’s borrowing costs, taking some pressure off the national budget.

-

Commercial Papers: As the yield on risk-free T-Bills drops, the yields on corporate CPs will likely follow. The credit spread—the extra bit of yield investors want for holding company debt over government debt—might also shrink as confidence in the Nigerian business environment grows. This means cheaper short-term funding for Nigeria’s top

companies.

This could also have a nice knock-on effect on Nigeria’s sovereign credit rating. Global rating agencies like Moody’s and Fitch see better FATF compliance as a sign of stronger institutions and better governance. Moody’s had already upgraded Nigeria’s outlook to positive in May 2025, thanks to the government’s reform efforts. The FATF delisting adds more fuel to this fire and could lead to further upgrades, creating a positive feedback loop of better creditworthiness and lower borrowing costs.

A New Playing Field for Everyone

The delisting will change the day-to-day reality for all the key players in the money market.

For the Central Bank of Nigeria (CBN): The FATF’s decision is a big thumbs-up for the CBN’s recent policy moves, especially those aimed at making the financial system more transparent and well-supervised. A steadier flow of foreign currency will ease the pressure on the country’s reserves, giving the CBN more wiggle room in managing monetary policy and the exchange rate.

For Commercial Banks: The benefits for the banking sector are instant and massive. With the grey-list stigma gone, dealing with international partner banks will become smoother and cheaper. The need for extra-cautious due diligence will disappear, cutting compliance costs and speeding up international transactions like trade finance and remittances. This improved access to global financial system will make it easier for them to serve their clients and manage their own international cash flow.

For Companies Issuing Debt: The delisting could breathe new life into the corporate debt market. Before, high T-Bill yields were pushing private borrowers out of the way. With government borrowing costs expected to fall, CPs will look more attractive to investors chasing a better. This along with more cash in the market will make it easier for companies to use the CP market for their short-term funding, giving them a vital and more affordable alternative to bank loans.

Crunching the Numbers: How the Market Reacted

Talk is cheap, but the market data tells a compelling story. By looking at the key numbers for T-Bills and CPs before and after the big announcement in October 2025, we can see a real shift in mood, demand, and borrowing costs.

The data below shows a clear and positive reaction, with government borrowing rates falling and the corporate funding scene looking much healthier, backing up everything we’ve discussed.

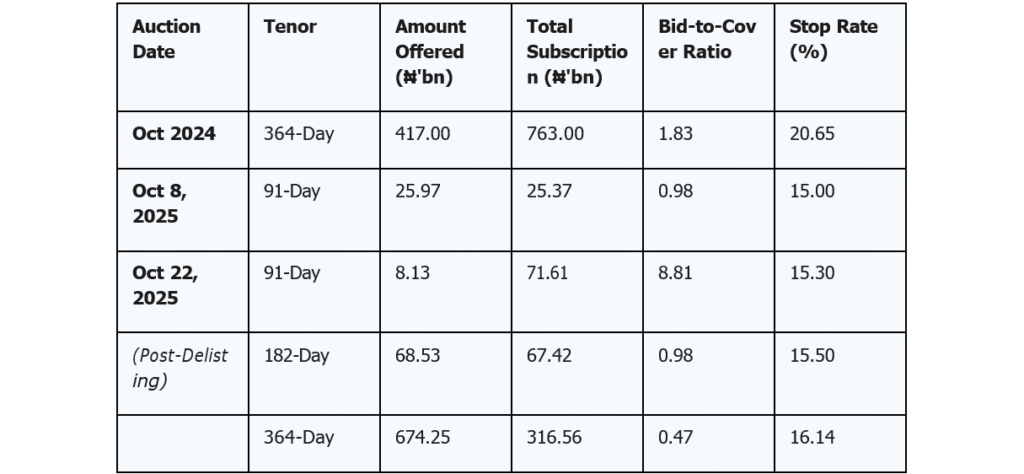

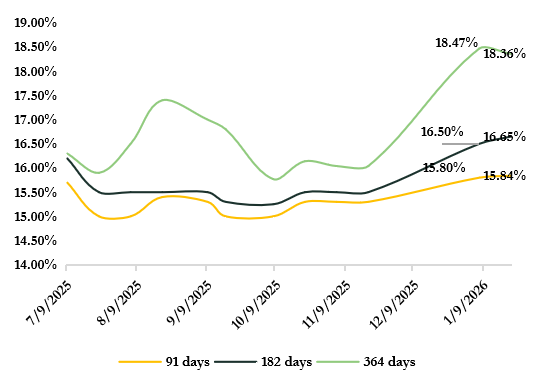

Table 1: A Look at Nigerian Treasury Bill Auctions (Q4 2024 – Q1 2026)

This table compares the results of T-Bill auctions around the time of the FATF delisting. The key things to watch are the Stop Rate (the effective yield and the government’s borrowing cost) and the Bid-to-Cover Ratio (how many bids were received for every naira on offer), which shows investor appetite.

What the T-Bill Numbers Tell Us:

The data shows a hefty drop in government borrowing costs right after the delisting news. The rate for the main 364-day T-Bill was a steep 20.65% in October 2024, reflecting the high-risk mood and tight money supply at the time. By the auction on 22 October 2025, just before the official announcement, that rate had already fallen to 16.14%. While cooling inflation and changing expectations about central bank policy also played a part, the delisting was a major catalyst. The massive jump in the bid-to-cover ratio for the 91-day bill in the 22 October auction (from 0.98 to a whopping 8.81) shows a huge surge in investor demand, likely as people got wind of the good news. This combo of falling rates and soaring demand is solid proof that the market gave Nigeria’s clean bill of health a big thumbs-up.

Table 2: A Snapshot of the Nigerian Commercial Paper Market (H1 2025)

The health of the Commercial Paper market is a great indicator of how easy it is for companies to get funding. This table shows some of the big CP deals in the first half of 2025, in the run-up to the delisting.

What the CP Market Tells Us:

The CP market was buzzing in the lead-up to the delisting, with Nigerian companies raising over ₦330 billion in the first quarter of 2025 alone. This shows that even with high interest rates, the CP market was a vital source of cash. The data also shows how much this cash cost. An MTN Nigeria CP issued in late 2024, when uncertainty was at its peak, came with a hefty 29.00% yield. By mid-2025, other companies like Jawa International and Skymark Partners were getting funding at rates in the 22-23% range. This suggests that corporate borrowing costs were already starting to ease as the market got better and confidence in Nigeria’s reforms grew. The delisting is set to speed up this trend, making CPs an even better deal for Nigerian businesses and helping this part of the money market to grow even stronger.

The Road Ahead: Strategy and Advice

Getting off the FATF grey list is a massive win for Nigeria, completely changing the game for its money market. But to make the most of this opportunity, everyone needs to be smart about what comes next. This means understanding the opportunities, spotting the risks, and having a clear game plan.

The Next 12-24 Months

The medium-term outlook is bright, but with a few ‘ifs’. The initial wave of good feeling and lower risk premiums should continue, making for a more stable and liquid market. The key thing to watch over the next year or two will be the tug-of-war between this positive momentum and what happens with Nigeria’s own economic policies.

A big piece of the puzzle is the 12-month “probation” period set by the FATF. During this time, Nigeria has to prove that its reforms weren’t just for show and are actually working day-to-day. Getting through this period successfully will be vital for locking in that newfound investor confidence. At the same time, what happens with inflation and the CBN’s interest rate decisions will still be major factors. If inflation keeps falling and the CBN feels it can start to lower the MPR, the downward trend in money market yields that the delisting started will get a serious boost.

Keeping the Ball Rolling: Risks and How to Dodge Them

The biggest risk is that everyone gets tired of all the hard work—a classic case of “reform fatigue.” The delisting can’t be seen as “mission accomplished”. If things slip back to the old, lax ways, Nigeria could find itself back on the grey list, and the damage to its reputation and economy would be huge.

To avoid this, the reforms need to become part of the furniture. This means:

-

Keeping the Team Together: The brilliant multi-agency teamwork led by the NFIU needs to become the new normal for fighting financial crime, not just a temporary.

-

Showing, Not Just Telling: The anti-corruption and regulatory bodies need to keep showing their teeth by investigating and prosecuting major financial crimes, proving that the new laws are being used.

-

Staying in the Loop: Nigeria needs to keep talking to the FATF and its regional partner, the Inter-Governmental Action Group Against Money Laundering in West Africa (GIABA), to stay up-to-date with global standards and show it’s still commifled.

A To-Do List for the Key Players

To grab the opportunities on offer, here’s what the main players should be thinking about:

For Investors: It’s time to rerun the numbers. Both international and local investors should take a fresh look at the risk premium they attach to The delisting means it should be lower, which might uncover some bargains in Nigerian fixed-income assets. Keep a close eye on T-Bill auctions for good entry points as yields fall, and check out the growing CP market, especially for issues from companies with solid credit ratings.

For Policymakers (CBN, DMO, Ministry of Finance): The government needs to be open and clear about its progress during the probation period to build on the investor confidence it has They should use the new environment of lower borrowing costs to manage the national debt more effectively. And crucially, they must make sure that new tools like the Beneficial Ownership Register are actively used to investigate crimes, sending a strong message to anyone thinking of trying anything dodgy.

For Company Finance Chiefs: This is a golden opportunity. Finance teams should be reviewing their short-term funding plans right now. The CP market is now more liquid, easier to access, and potentially cheaper than it was before the delisting. Companies should get ready to issue CPs by obtaining an investment-grade credit rating and talking to financial advisors to take advantage of the better market conditions. This is a smart way to diversify funding away from just relying on bank loans and to lower the overall cost of capital.

👍🏼