- Report

FEBRUARY INFLATION REPORT

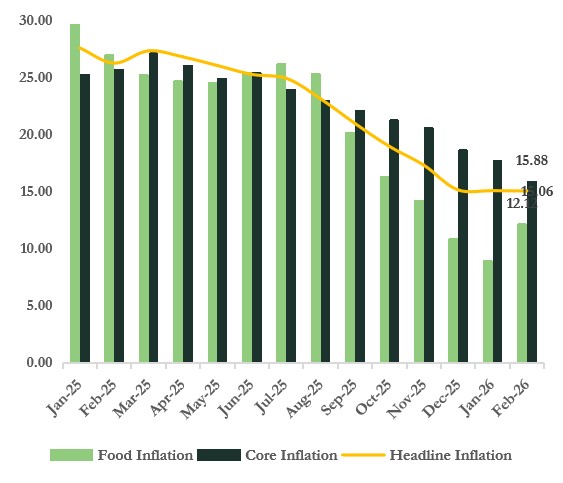

Headline Inflation Eases to 15.06% in February but Monthly Pressures builds.

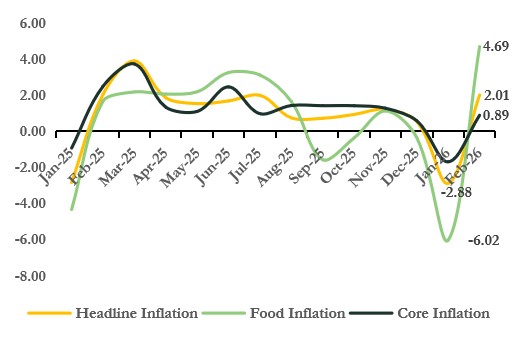

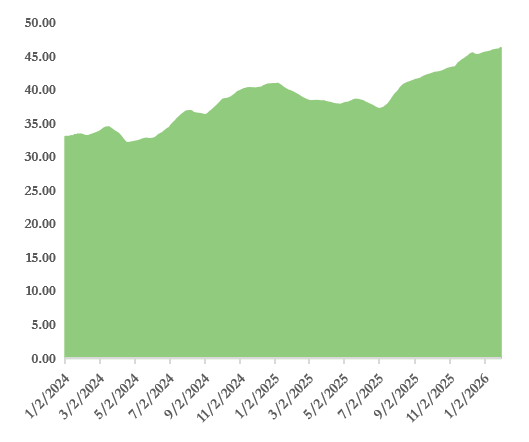

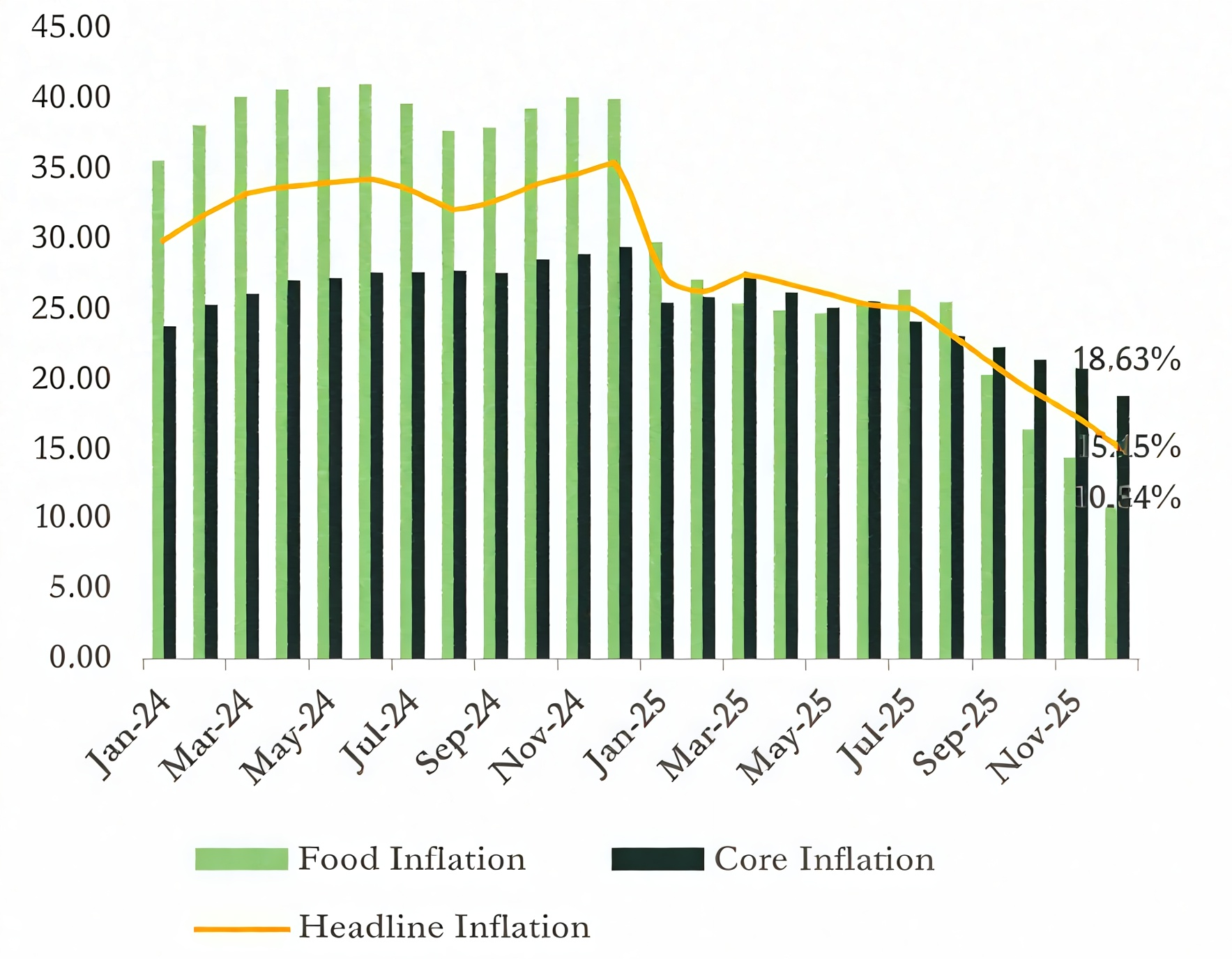

According to the National Bureau of Statistics, headline inflation in Nigeria eased marginally to 15.06% in February 2026 from 15.10% in January, marking an 11th consecutive month of disinflation. The moderation was driven by a decline in core inflation (15.88% from 17.72%), which offset the increase in food inflation (12.12% from 8.89%). On a month-on-month basis, headline inflation rose to 2.01% from -2.88%, indicating a short term rebound in price pressures

Disaggregated data shows that food inflation accelerated to 12.12% from 8.89% in January. Similarly, on a month–on– month basis, food inflation accelerated to (4.69% from a 6.02%) deflation recorded in January, the highest since rebasing, reflecting tightening food supply conditions as post-harvest gains fade and the farmers transition into the planting season. Additionally, persistent security and logistics constraints affect distribution to key consumption centers

Core inflation, which excludes volatile agricultural produce and energy, moderated to 15.88% vs 17.72% in January, but rose to (0.89% vs -1.69%), m-o-m, suggesting renewed underlying pressures. This uptick was driven by increases in the rent index (3.07% vs 0.72%) m-o-m, alongside a moderation in deflation within the transport (-0.26% vs -1.02%) m-o-m and restaurant components (1.12% vs -0.08%) m-o-m

OUTLOOK

Inflation is expected to edge higher in March 2026, potentially interrupting the recent disinflation trend. The disruption in the Strait of Hormuz amid tensions between the United States and Iran has elevated global oil prices, translating into higher domestic fuel costs (₦ 1250/per liter) and transportation expenses. In addition, the temporary depreciation of the naira is likely to increase imported inflation through exchange rate pass-through. Consequently, both food and core inflation are expected to rise modestly in the near term, with headline inflation likely to tick up slightly before stabilising, if energy and exchange rate pressures ease.

Y-o-Y Inflation Trend

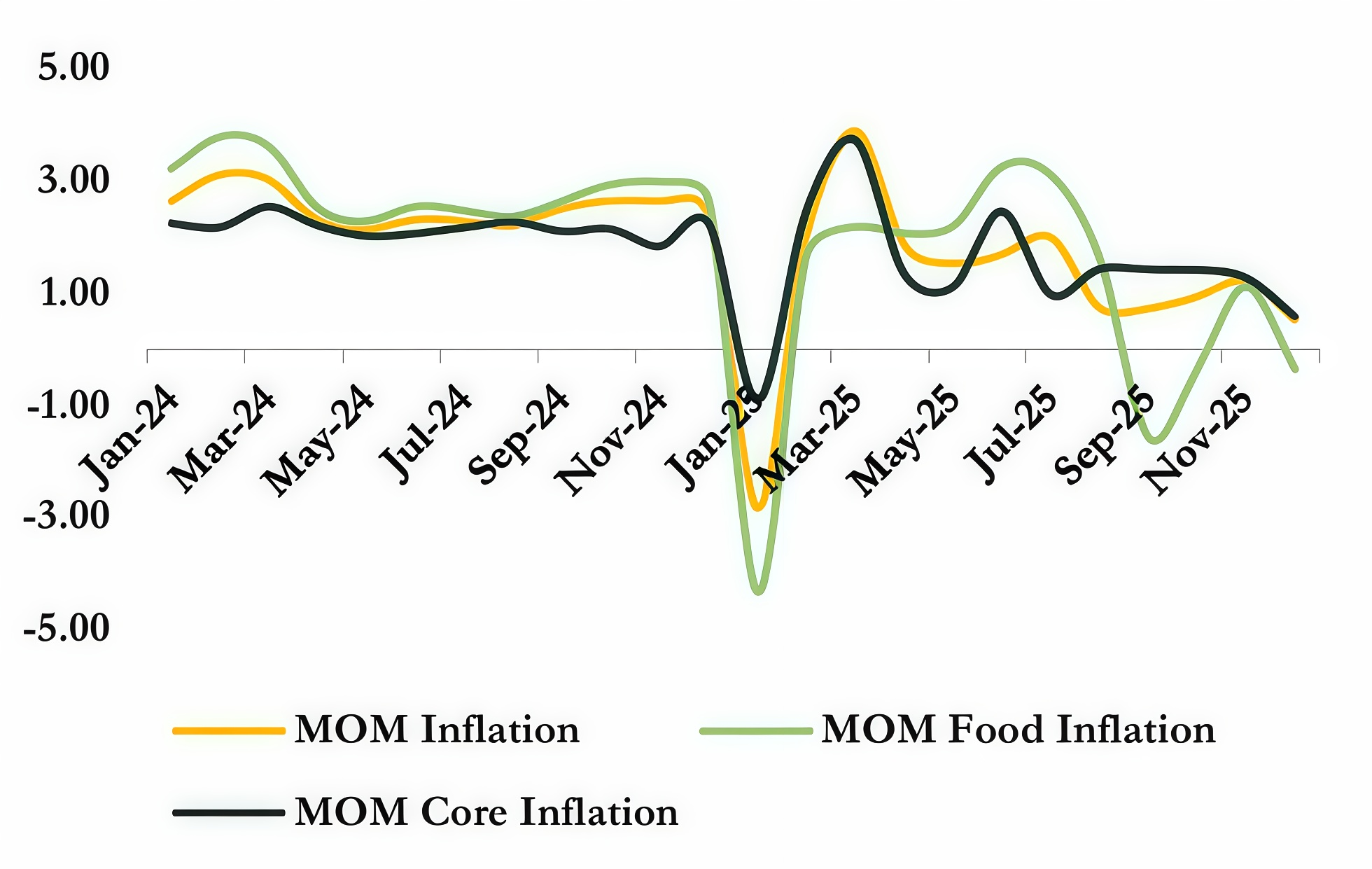

M-O-M Inflation Trend

- Insights

BRB Monthly Market Report January 2026

MACROS

Nigeria’s macroeconomic landscape in January 2026 reflected a clear shift toward stabilization, supported by moderating inflation, improving foreign exchange dynamics, and growing international confidence in the reform trajectory of the economy. These developments provided a supportive backdrop for domestic financial markets and reinforced expectations of a more balanced macroeconomic environment in 2026.

Inflation dynamics improved during the period, with headline inflation moderating to 15.15% in December 2025 from 17.33% in November, according to the National Bureau of Statistics. This decline was largely

driven by the adoption of a revised Consumer Price Index methodology, which rebased the index to 2024 and transitioned to a 12-month average reference period. Under the previous 2009 methodology, inflation would have remained significantly higher, underscoring the technical component of the observed disinflation.

Nonetheless, underlying price pressures also eased, with food inflations lowing for the fifth consecutive month to 10.84%, supported by seasonal harvest effects and a firmer naira, while core inflation declined to 18.63% from 20.59%, reflecting reduced pass-through from exchange rate pressures.

Inflation Trajectory

In the foreign exchange market, stability at the Nigerian Foreign Exchange Market (NFEM) window improved noticeably in January. The naira strengthened toward the end of the month, closing within

the ₦1,386/$ to ₦1,401/$ range, as foreign portfolio inflows increased and liquidity conditions improved. Attractive domestic yields, coupled with enhanced confidence in policy direction, encouraged offshore participation in the fixed income market, easing demand pressures on the currency. This was further supported by improved supply from exporters and market participants, reinforcing near-term exchange rate resilience

Economic activity indicators also pointed to strengthening momentum. The Central Bank of Nigeria’s composite Purchasing Managers’ Index rose to 57.6 points in December 2025, marking the fastest pace of expansion in nearly five years and extending the expansionary trend to thirteen consecutive months.

Growth was broad-based across sectors, with agriculture leading, followed by strong recoveries in industrial output and services activity. The PMI data suggest improving business confidence and strengthening domestic demand entering 2026.Nigeria’s international financial standing improved further during the month, following its formal removal from the European Union’s list of high-risk third countries for money laundering and terrorism financing, effective January 29, 2026. This development followed Nigeria’s earlier exit from the Financial Action Task Force grey list in October 2025 and represents a significant milestone in restoring global credibility. The delisting is expected to reduce transaction friction for cross-border flows, improve correspondent banking relationships, and broaden the base of international investors engaging with Nigerian assets.

The improving macro narrative was reinforced by the International Monetary Fund’s upward revision of Nigeria’s 2026 growth forecast to 4.4% in its January World Economic Outlook update. The revision reflects confidence in ongoing structural reforms, improved macroeconomic coordination, and stronger productivity across agriculture, manufacturing, and services. Nigeria is now positioned as a notable contributor to global growth in 2026, with an outlook that compares favorably to several peer economies.

External buffers continued to strengthen, providing additional support to macro stability. Gross external reserves rose to approximately $46.1 billion by the end of January, up from $45.0 billion at the close of 2025. The improvement was driven by higher oil receipts, steady diaspora remittances, and sustained portfolio inflows. Forward projections suggest reserves could exceed $51billion by year-end, reinforcing the Central Bank’s capacity to manage currency volatility and absorb external shocks.

MACROS

Looking ahead to February 2026, inflation is expected to continue its gradual moderation, supported by base effects from the revised CPI methodology, stable exchange rate conditions, and easing food supply pressures. Headline inflation is likely to trend marginally lower or remain broadly stable in the near term. However, risks to this outlook include potential energy price shocks, changes to administered prices, or renewed exchange rate volatility, particularly if global commodity prices spike or domestic supply disruptions emerge.

The exchange rate is expected to remain relatively stable in February, with the naira likely to trade around the ₦1,400/$ level, supported by sustained portfolio inflows, improved reserve buffers, and ongoing price discovery at the NFEM window. Nonetheless, downside risks persist, including the possibility of capital flow reversals if global financial conditions tighten, heightened geopolitical tensions affecting oil markets, or delays in oil production recovery. Maintaining confidence in policy consistency and reform implementation will remain critical to preserving near-term currency stability.

The macroeconomic environment entering February 2026 reflects an improving balance, with stabilization increasingly anchored by structural reforms rather than temporary market interventions. While vulnerabilities remain, the convergence of moderating inflation, strengthening external buffers, and rising international confidence provides a more resilient foundation for economic and financial market performance in the months ahead.

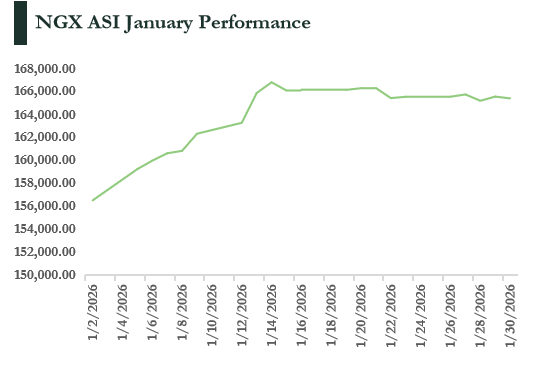

The Nigerian equities market began 2026 on a relatively positive footing, extending the bullish momentum seen in late 2025. This performance was underpinned by improving macroeconomic signals that suggested early signs of economic stabilization, alongside renewed investor confidence. As a result, total market capitalization on the Nigerian Exchange (NGX) increased by ₦6.8 trillion during January, closing at ₦106.15 trillion compared to ₦99.38 trillion at the end of December 2025

This 6.8% month-on-month expansion was largely driven by price appreciation in major blue-chip stocks, complemented by fresh capital inflows through primary market activities. Reflecting these gains, the NGX All-Share Index (ASI) delivered a strong start to the year, recording both month-to-date and year-to-date returns of 6.27% to close January at 165,370.40 points.

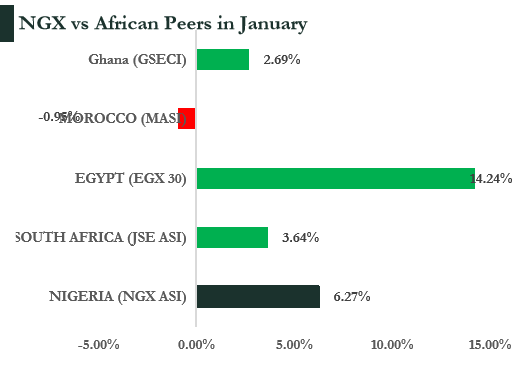

This performance was not an isolated development but broadly aligned with trends across global and Pan-African equity markets. Notably, the NGX outperformed several African peers, including the BRVM and the Moroccan exchange, which recorded more muted starts to the year.

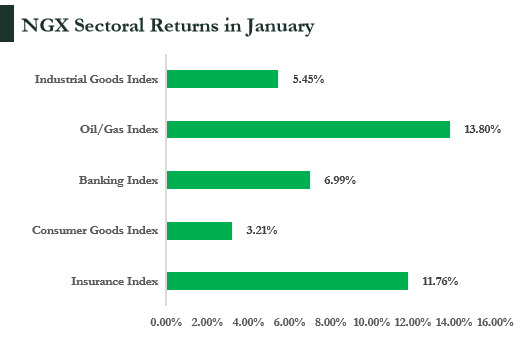

Sectoral performance on the NGX in January 2026 largely reflected the broader market’s bullish tone, with most indices closing the month in positive territory as investors selectively rotated into high-conviction sectors. The Oil and Gas index emerged as the top performer, advancing by 13.80%, driven by price gains in key integrated energy stocks such as SEPLAT (+15.34%) and ARADEL (+16.45%). Institutional confidence was further reinforced by improved governance sentiment following strategic board appointments, including the induction of Mr. Tony Elumelu to Seplat Energy’s board.

The Insurance index followed closely, rising by 11.76% on the back of ongoing recapitalization efforts and broad-based price appreciation across the sector. Notable gainers included NEM Insurance (+19.40%), AIICO (+10.82%), Veritas Kapital (+43.27%), and Mutual Benefits Assurance (+34.84%), reflecting improving sentiment toward balance sheet strengthening and earnings recovery prospects.

The Banking index posted a solid 6.99% gain, supported by renewed interest in fundamentally strong lenders such as GTCO (+9.15%), Zenith Bank (+15.61%), Wema Bank (+14.71%), and Access Holdings (+7.62%), as investors positioned for resilient earnings and attractive dividend yields. Similarly, the Industrial Goods index advanced by 5.45%, driven largely by gains in Dangote Cement (+4.27%) and Lafarge Africa (+16.73%), amid sustained demand expectations within the construction value chain.

Meanwhile, the Consumer Goods index added 3.21%, extending its steady appreciation after emerging as the bestperforming sector in 2025. Gains in Nestlé Nigeria (+10.00%), Cadbury Nigeria (+11.85%), Unilever Nigeria (+8.33%), and Dangote Sugar (+8.33%) underscored continued investor preference for companies with relatively strong pricing power and improving margin outlooks.

Despite the NGX All-Share Index delivering a 6.27% return in January, stock-level performance was highly dispersed, creating meaningful alpha opportunities for active managers. Several mid- and small-cap stocks recorded outsized gains, driven by sector repositioning, low-float dynamics, and renewed speculative interest. Deap Capital Management & Trust Plc (+394.21%) and SCOA Nigeria Plc (+345.07%) led the advancers, while strong performances were also recorded in NCR Nigeria Plc (+173.73%), Zichis Agro Allied Industries Plc (+131%), particularly notable as a recent IPO, and Multiverse Mining, supported by improving sentiment in the mining and basic materials sector.

On the downside, a small number of stocks underperformed, largely due to profit-taking following extended rallies rather than fundamental weakness. Ikeja Hotel Plc (-23.03%) declined as investors locked in gains in the hospitality sector, while Juli Plc (- 9.93%) and Austin Laz (-8.24%) faced selling pressure amid rotation within the retail and services space. Conoil Plc (-9.72%) also recorded a modest pullback, standing out as a rare decliner within the Oil and Gas sector, with price weakness largely reflecting technical corrections.

Market direction in February is expected to be driven largely by the release of audited 2025 financial results and dividend announcements. Nigeria’s dividend season typically supports equity prices, as investors rotate toward fundamentally strong, high-yield stocks. The banking sector should remain the center of activity amid ongoing recapitalization, while potential large-scale listings, such as the anticipated Dangote Refinery IPO, present upside catalysts for market liquidity and capitalization. Continued traction on the Growth Board also points to a growing pipeline of SME listings, particularly in agriculture and technology. Macroeconomic risks remain centered on inflation trends and monetary policy. However, strong market capitalization and resilient earnings among large-cap stocks suggest the NGX is well positioned to sustain positive momentum into February 2026.

FIXED INCOME

Domestic Money Market and System Liquidity

The Nigerian fixed income market in January 2026 was characterized by ample system liquidity, shifting yield dynamics, and improved investor confidence following favorable macroeconomic developments.

Market sentiment was largely shaped by the moderation in headline inflation and the Central Bank of Nigeria’s decision to maintain a tight but stable monetary policy stance. These factors drove strong participation at primary market auctions and contributed to yield compression toward the latter part of the month.

A key catalyst was the National Bureau of Statistics’ release of December 2025 inflation data, which showed headline inflation easing to 15.15% from 17.33% in November. The decline was primarily attributed to revisions in the Consumer Price Index methodology, including rebasing to 2024 and the adoption of a 12- month average reference period. This perceived disinflationary trend supported fixed income demand and reinforced expectations of yield stabilization.

Against this backdrop, the CBN retained the Monetary Policy Rate at 27.0% at its January meeting, signaling policy continuity. The moderation in inflation expectations provided a tailwind for fixed income instruments, particularly at the long end of the Treasury curve, as investors increasingly priced in lower real yield pressures.

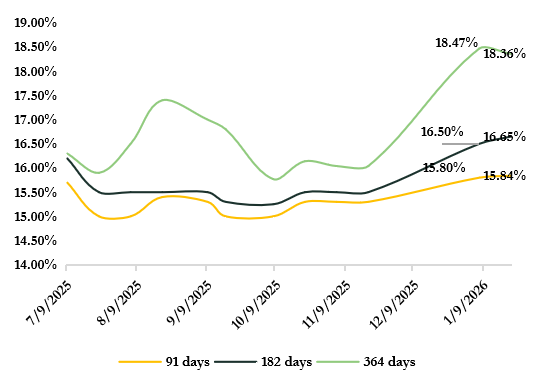

In the Treasury bills primary market, investor demand remained robust throughout the month. At the January 7 auction, the CBN offered ₦1.15 trillion across the 91-day, 182-day, and 364-day tenors, attracting total subscriptions of ₦1.54 trillion and a bid-cover ratio of 1.35x. Although stop rates increased across all tenors, clearing at 15.80%, 16.50%, and 18.47%, respectively, strong participation

underscored sustained appetite for short-dated government securities.

Demand intensified at the January 21 auction, where ₦1.15 trillion was again offered. Total subscriptions surged to ₦3.44 trillion, translating to a bid-cover ratio of 3.24x, with particularly strong interest in longer-dated bills. While stop rates for the 91-day and 182-day instruments edged higher to 15.84% and 16.65%, the 364-day bill cleared lower at 18.36%, reflecting growing investor preference for duration. The

relatively low allotment rate suggests that unmet bids are likely to flow into the secondary market.

Eurobonds and Global Confidence

Nigerian Eurobonds traded with mixed-to-moderately positive sentiment in January 2026, shaped by a combination of global macroeconomic developments, geopolitical risks, and improving domestic fundamentals. Early in the month, investor sentiment was cautious amid heightened global risk aversion, driven by volatility in energy markets, geopolitical tensions in the Middle East, and supply disruptions caused by severe winter storms in the United States. These factors contributed to short-term oil price volatility, with Brent crude briefly trading above USD70/bbl as markets repriced supply risks.

Additional uncertainty stemmed from concerns around U.S. foreign policy actions, including interventions in Venezuela, which raised the prospect of disruptions to global oil supply. Given Nigeria’s continued reliance on oil revenues, sustained volatility in crude prices remained a key macro risk, influencing foreign investor positioning in Nigerian sovereign debt during the early part of the month.

Mid-month sentiment improved as U.S. Treasury yields eased and oil prices stabilized following their initial spike. Softer U.S. jobless claims and the U.S. Federal Reserve’s decision to hold policy rates reinforced expectations of a prolonged pause through most of H1 2026, following cumulative rate cuts in late 2025. This shift supported renewed demand for emerging market debt, leading to modest yield compression across Nigerian Eurobonds.

By the latter half of January, buying interest strengthened, driving the average benchmark Nigerian Eurobond yield down to approximately 7.12%. However, profit-taking ahead of key global macro events and renewed upward pressure on U.S. Treasury yields toward month-end resulted in mild volatility, with the benchmark yield ticking higher to around 7.23% in the final trading sessions. Nigerian Eurobonds closed the month slightly weaker on a month-on-month basis, reflecting cautious investor positioning amid persistent global uncertainty.

FIXED INCOME

A major positive development during the month was Nigeria’s formal removal from the European Union’s list of high-risk third countries for money laundering and terrorism financing, which took effect on January 29, 2026. This followed Nigeria’s earlier exit from the Financial Action Task Force (FATF) grey list in October 2025, representing a significant improvement in the country’s international financial standing. The delisting is expected to reduce compliance costs for cross-border transactions, enhance correspondent banking relationships, and foster broader participation by foreign portfolio investors in Nigeria’s fixed income and Eurobond markets in the medium term.

OUTLOOK

The Nigerian fixed-income market is set for a gradual recalibration. With the CBN maintaining tight monetary conditions and ample liquidity, short-term NTB yields are expected to ease, providing investors with opportunities to secure attractive returns ahead of potential rate adjustments. Demand for longer-dated government bonds remains robust, supported by stable coupon payments and potential capital appreciation in a moderating yield environment.

Fiscal discipline and strategic debt management will be key. A shift toward lower-cost, long-dated instruments, including diaspora bonds, Sukuk, or green bonds, combined with efforts to diversify non-oil revenues, could enhance debt sustainability and bolster investor confidence. This outlook depends on continued macro stability, easing inflationary pressures, and contained external debt risks.

On the external front, while Eurobond issuances have drawn strong demand, global rate dynamics and geopolitical risks could pressure yields, underscoring the need for vigilance. Overall, highyield, long-term government debt and Tbills is likely to remain a preferred allocation in the near to medium term, contingent on stable macro fundamentals and consistent policy execution.

- Report

December 2025 Inflation Report

Inflation eased to 15.15% in December 2025 following an adjustment by the NBS.

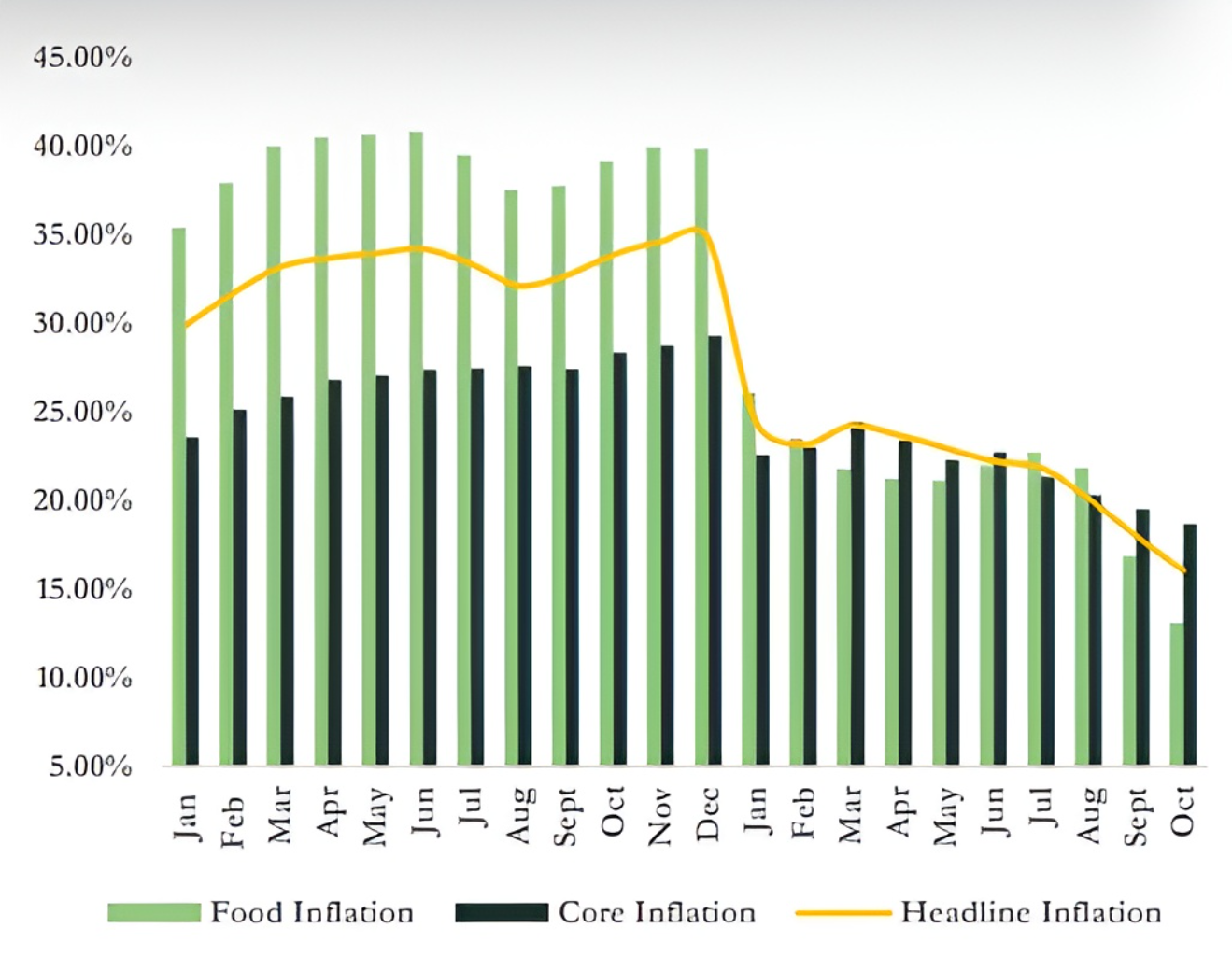

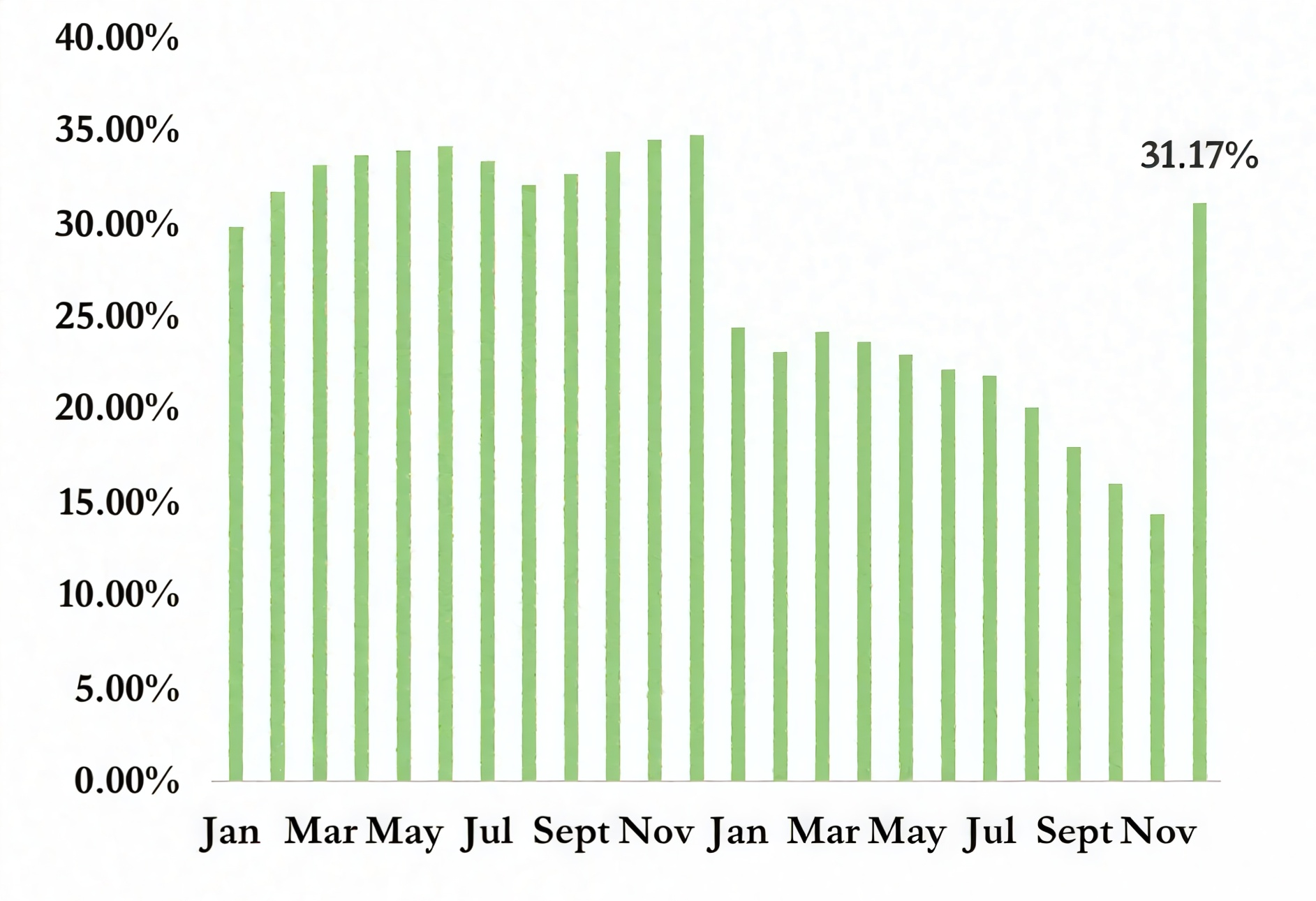

Nigeria’s headline inflation moderated to 15.15% year-on year in December 2025, down from 17.33% in November, reflecting a methodological adjustment by the National Bureau of Statistics (NBS).

The decline follows the NBS’s adoption of a 12-month average CPI for 2024 as the reference period, replacing the previous single-month (December 2024) base. This change was implemented to eliminate an artificial inflation spike caused by base effects. Under the former methodology, headline inflation for December 2025 was projected to surge to about 31.2%, a distortion driven by the comparison base rather than a sharp acceleration in underlying price pressures. The revised approach, therefore, provides a more accurate representation of inflation dynamics, even as price levels remain elevated.

On a disaggregated basis, food inflation eased to 10.84% in December from 14.21% in November, while core inflation moderated to 18.63% from 20.59%, reflecting a broad based slowdown in price momentum following the methodological adjustment. On a month-on-month basis, headline inflation decelerated to 0.54%, down from 1.22% in the prior month. Food inflation turned negative at 0.36%, compared with 1.13% in November, suggesting easing short-term price pressures, while core inflation slowed to 0.58% from 1.28% previously.

OUTLOOK

We expect headline inflation to maintain a downward trajectory in 2026, supported by a relatively stable exchange rate, which should help moderate imported inflation pressures. Additionally, a weaker global oil market, driven by a projected supply surplus, could further ease global energy prices. However, this presents a double-edged risk: while lower energy prices may reduce domestic fuel costs and ease transportation and logistics expenses, weaker oil prices could also dampen export earnings and exert pressure on the naira, potentially offsetting gains through higher import costs.

On balance, the anticipated disinflation trend may create room for the Monetary Policy Committee to begin a gradual pivot away from its current hawkish stance, should macroeconomic conditions remain supportive.

Y-o-Y Inflation Trend New CPI Series

Y-o-Y Inflation Trend Old CPI Series

M-O-M Inflation Trend New CPI Series