MACROS

Disinflation and FX Stability Strengthen Market Confidence

Nigeria’s macroeconomic landscape underwent a decisive re-anchoring in October 2025, driven by sustained disinflation, improved FX stability, and major sovereign risk reductions. The removal of Nigeria from the FATF grey list marked a critical turning point, materially lowering compliance friction for cross-border transactions and restoring investor confidence in the country’s financial governance architecture. These structural improvements, underpinned by renewed access to Eurobond markets, strengthened external buffers and provided a more predictable macroeconomic environment for both domestic and offshore investors.

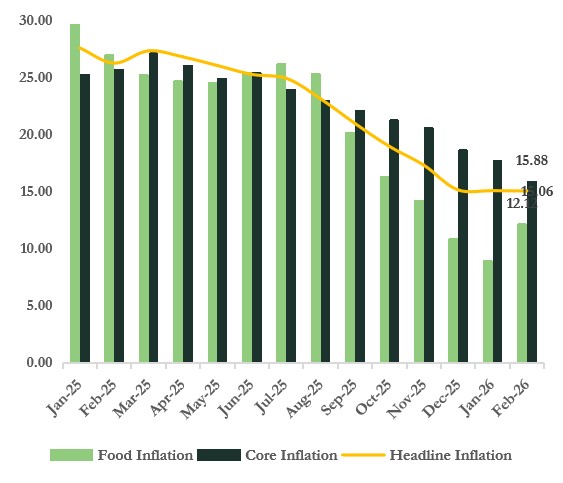

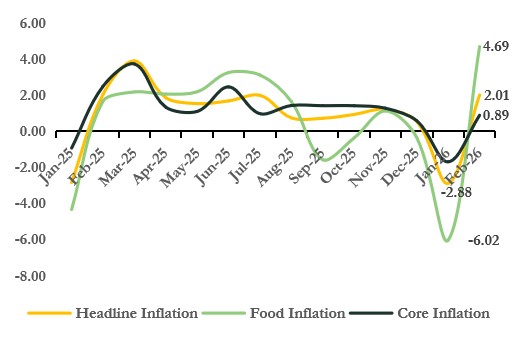

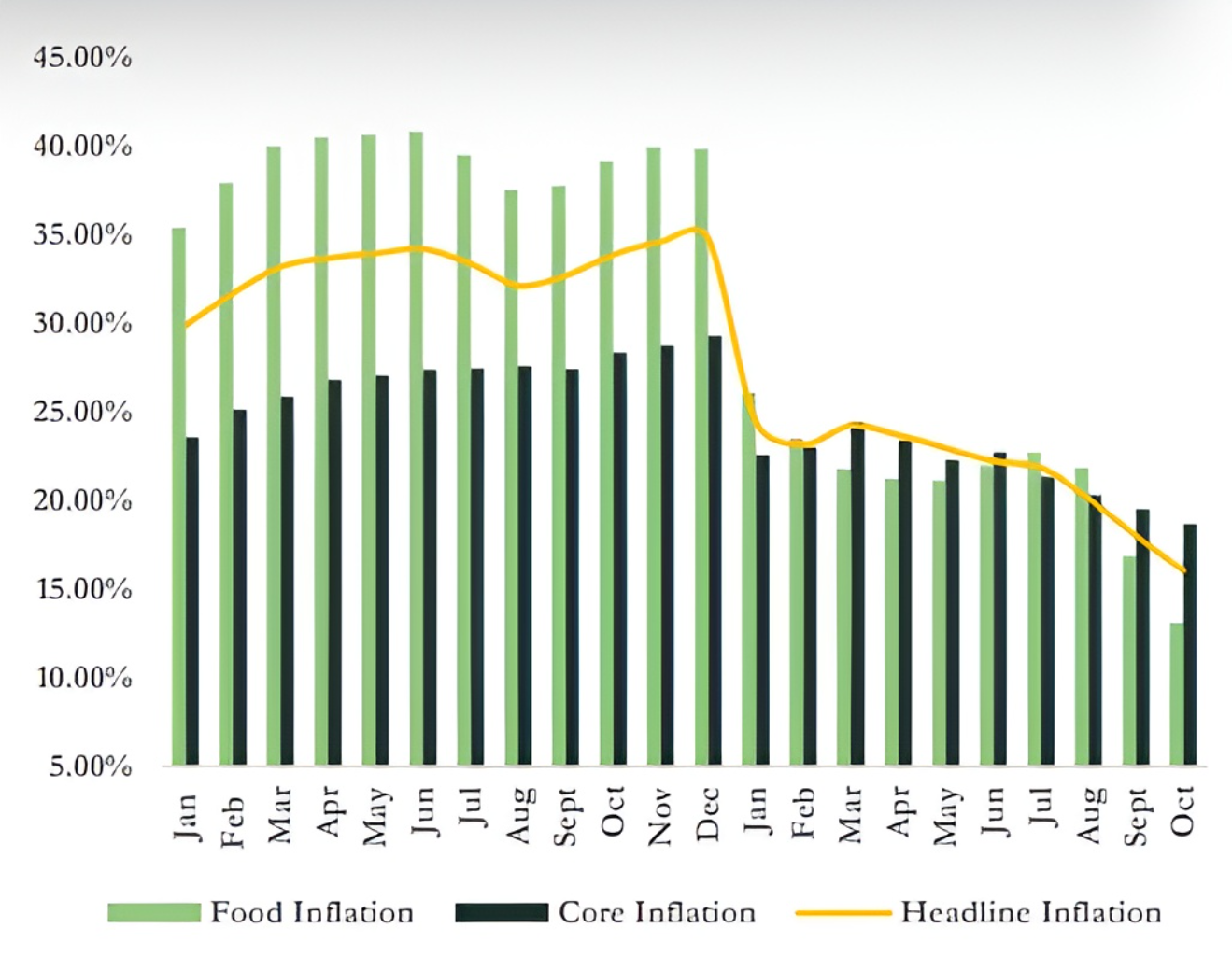

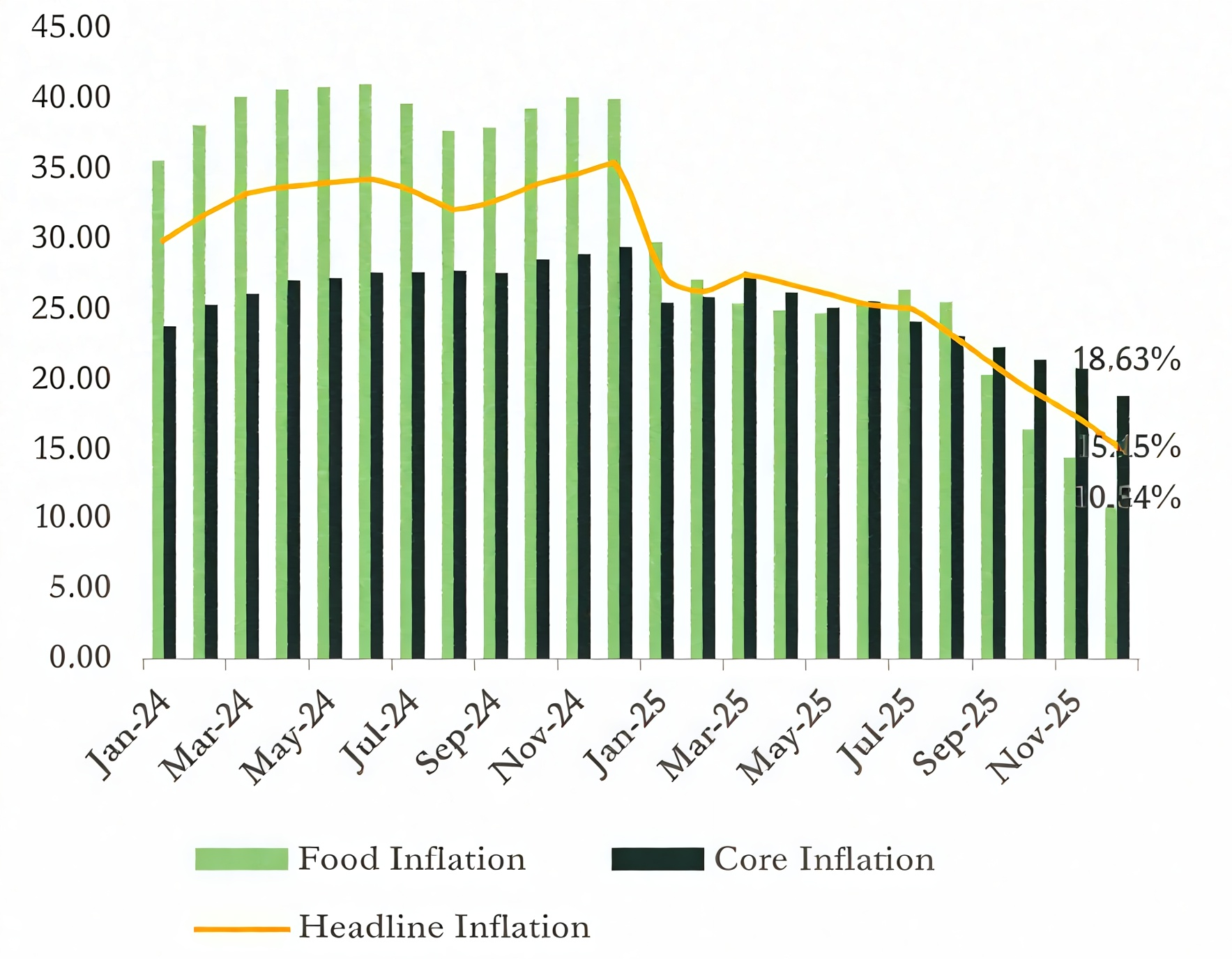

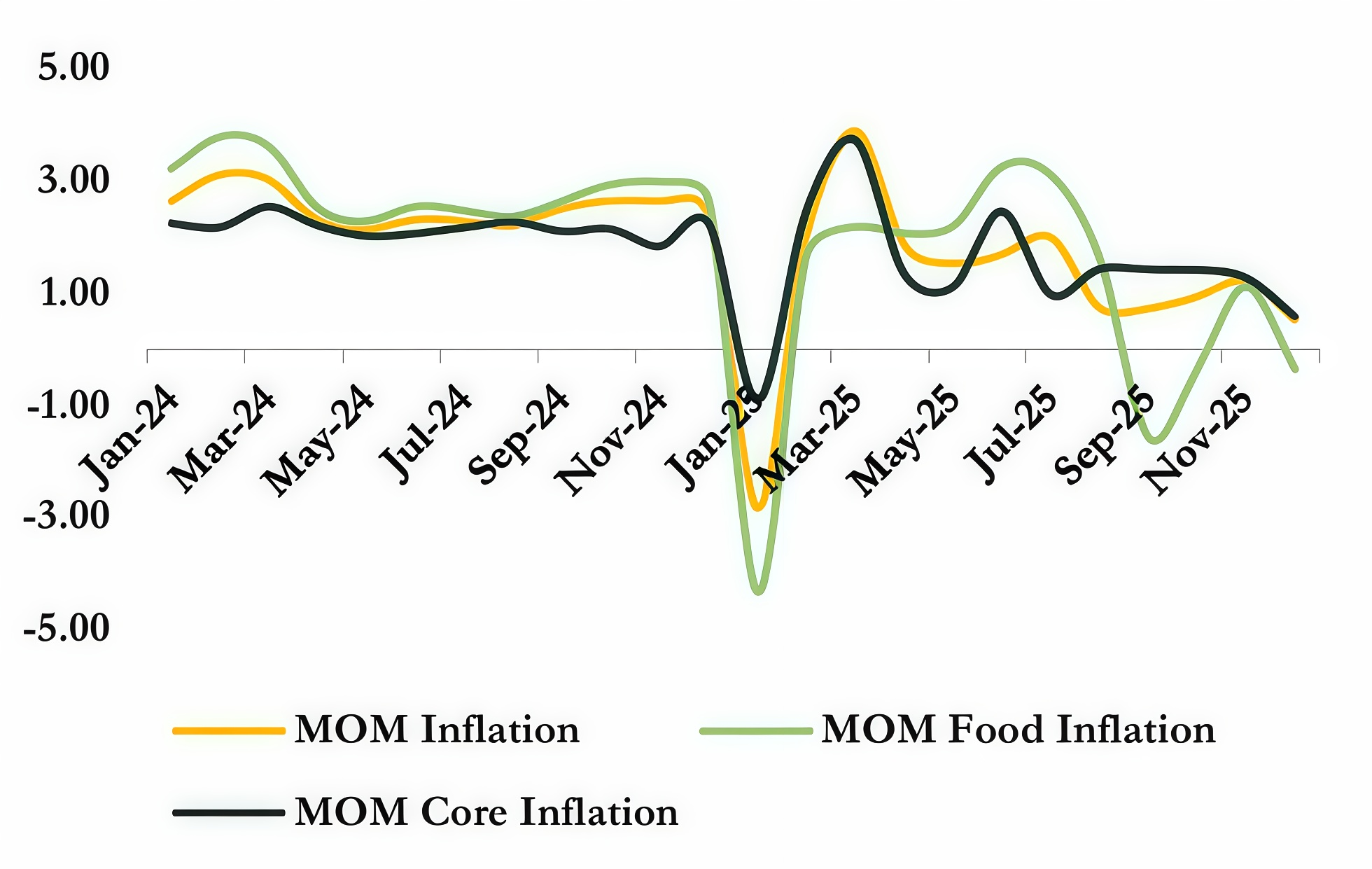

Disinflation remained the centerpiece of market confidence, with headline inflation moderating for the sixth consecutive month to 18.02%, its lowest level since mid-2022. Food and core inflation continued to soften, reflecting reduced currency pass-through and more stable price formation. Through this period, the CBN maintained a tight monetary stance, holding the MPR at 27.00% and preserving a strong positive real interest rate. This combination of anchored FX markets and high real returns sustained robust foreign portfolio inflows and reinforced expectations that Nigeria is nearing the end of its monetary tightening cycle.

Inflation Trajectory

FX Driven by Reserve Accumulation and Cautious Policy Easing

The Nigerian currency market in October 2025 consolidated its stabilization trend, supported by improved foreign exchange liquidity, strengthened external reserves, and a cautiously moderated monetary stance from the Central Bank of Nigeria. Throughout the month, th Naira maintained a firm performance in the Nigerian Foreign Exchange Market, benefitting from sustained inflows and a more orderly price formation environment. The official exchange rate appreciated modestly, closing October at approximately ₦1,421 per U.S. Dollar, marking one of its strongest levels since the operationalization of the electronic FX trading framework. This reflected the combined effect of improved supply conditions and heightened investor confidence following Nigeria’s reinforced macro stability narrative.

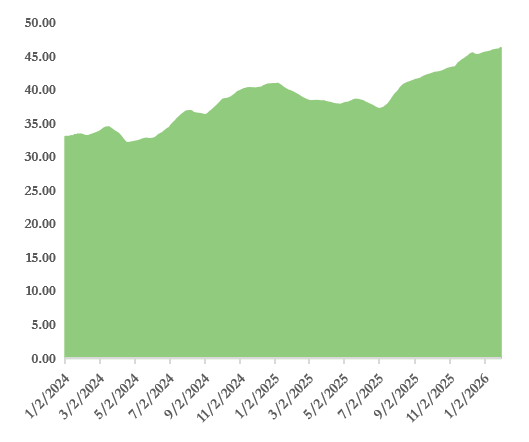

Gross FX Reserves ($’ billions)

The availability of FX in the official market was bolstered by rising capital importation, particularly Foreign Portfolio Investment attracted to Nigeria’s positive real interest rate environment, and improved dollar inflows from the oil sector, which recorded a notable recovery during the year. These fiscal adjustments complemented monetary tightening to reinforce a more balanced foreign exchange liquidity profile.

A critical anchor for the Naira’s stability during the month was the continued accumulation of external reserves. Gross external reserves strengthened from roughly $42.26 billion at the end of September to an estimated $43.15 billion at the close of October, reflecting almost $900 million in net reserve accretion. This improvement enhanced the central bank’s capacity to meet legitimate FX demand and significantly reduced speculative pressures in both the official and parallel markets. The strengthened reserve position also supported the broader policy narrative that Nigeria’s external balances were becoming more resilient, a development that reinforced confidence across the investment community.

Although the Central Bank did not convene a Monetary Policy Committee meeting in October, market conditions continued to adjust to the earlier reduction in the Monetary Policy Rate to 27.00%. The September rate cut, the first in five years, signalled a cautious shift toward policy easing, made possible by sustained disinflation and greater FX stability. Even with the reduction, the 27.00% MPR remained sufficiently high to maintain Nigeria’s competitive carry advantage, encouraging further portfolio inflows. The Cash Reserve Ratio remained elevated, absorbing substantial liquidity from the banking system and helping to maintain disciplined monetary conditions consistent with the central bank’s broader stabilization objectives.

EQUITIES

Sustained Bull Momentum and Strategic Capital Rotation

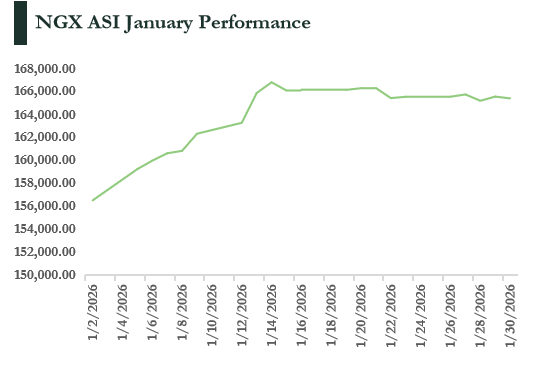

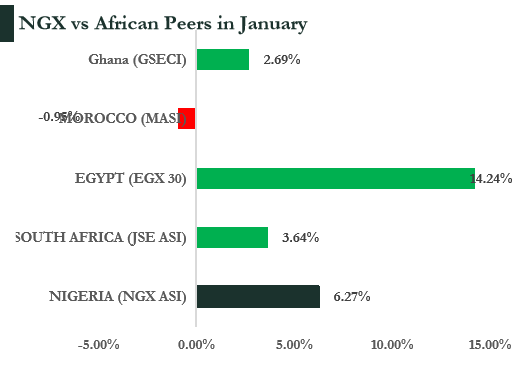

The Nigerian bourse (NGX) closed October 2025 on a bullish note, extending its strong year-long performance and ranking among the world’s best-performing equity markets. The month was driven by

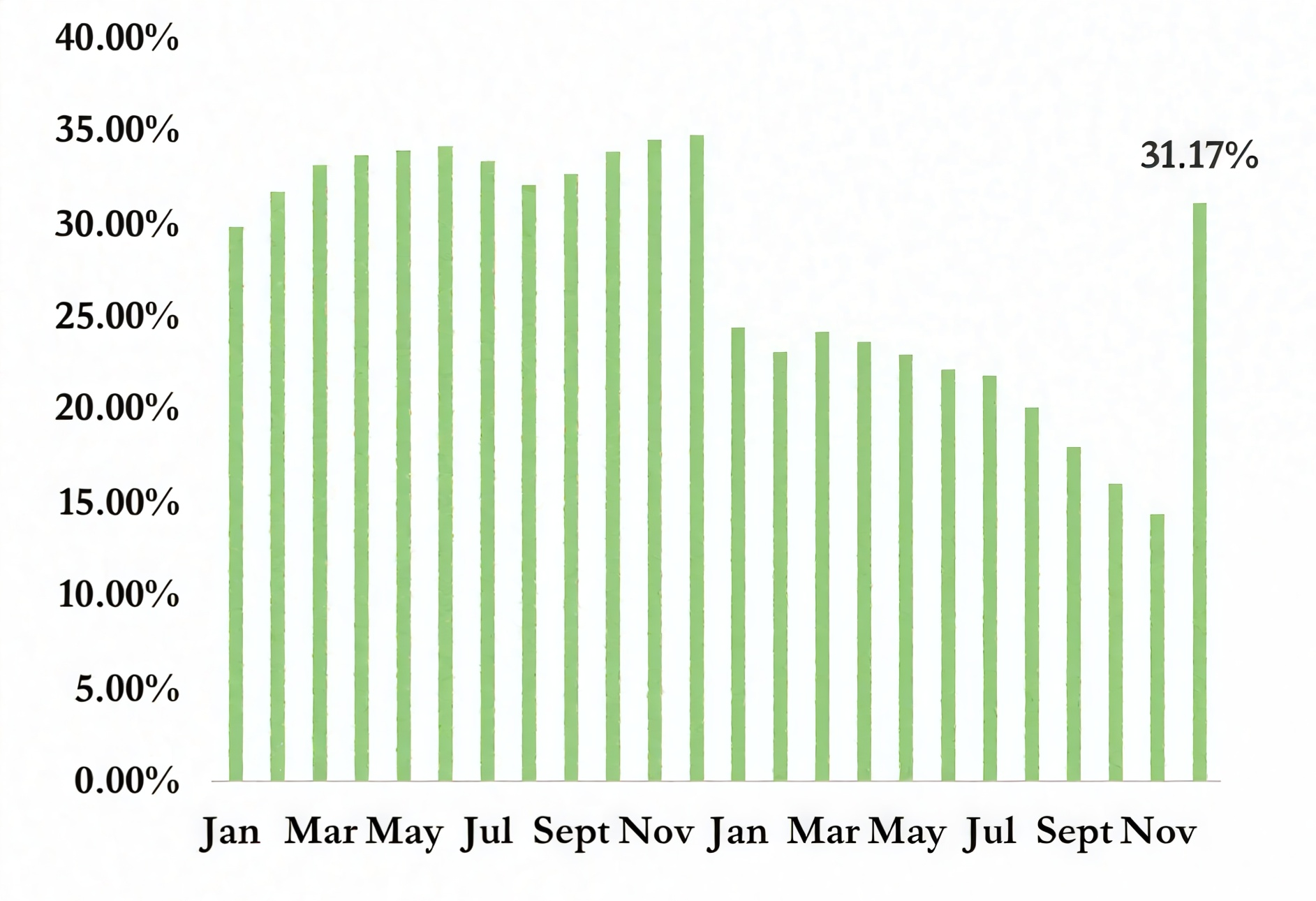

significant institutional capital rotation and renewed investor appetite for blue-chip stocks, whichmpushed the NGX All-Share Index (ASI) beyond the 150,000-point psychological threshold. The ASI rose by about 8.00% month-on-month (MoM) to close at 154,126.46 points, compared to a modest 1.72% gain in September. Consequently, market capitalization increased by ₦7.25 trillion, from ₦90.58 trillion in September to ₦97.83 trillion in October, reflecting substantial wealth creation within the period. This strong monthly advance accelerated the Year-to-Date (YTD) return to approximately 51.22%, up from about 41.80% in September, cementing the market’s leadership position globally.

This strong performance positioned October as the second-best month of 2025, behind the notable 16.57% rally recorded in July. The sustained rally highlights investors’ confidence in the resilience and value of Nigerian corporates despite high interest rates and declining fixed-income yields that would ordinarily divert liquidity away from equities.

NGX ASI Monthly Returns

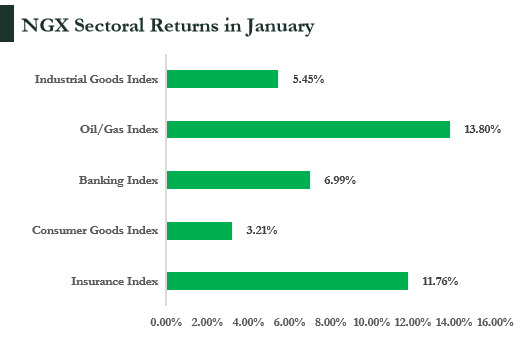

Sectoral performance in October 2025 was broadly bullish, reflecting a distinct flight to quality as investors rotated capital into sectors with stronger earnings visibility and defensive fundamentals. The Industrial Goods Index (+17.50%) led the market, buoyed by institutional accumulation in cement and manufacturing stocks such as Dangote Cement (+26.64%), WAPCO (+15.91%), and BUA Cement (+12.50%),

supported by positive Q3 earnings and improved sentiment following Dangote Cement’s expansion into the Ivory Coast.

Similarly, the Oil & Gas Index (+15.45%) benefited from rising global oil prices and large institutional trades concentrated in premium tickers like Aradel Holdings (+41.30%), Eterna (+29.08%), and Seplat (+10.00%), positioning the sector as a hedge against inflation and currency weakness. This suggests large-scale, sustained accumulation by major domestic institutional investors, such as pension funds, alongside possibly increased interest from sophisticated international investors seeking exposure to high-quality, fundamentally sound equity assets amidst global risk environments. This capital inflow demonstrates confidence that corporate earnings will continue to outpace macroeconomic volatility.

NGX ASI Historical Performance

The Consumer Goods Index (+4.85%) also advanced, driven by solid Q3 earnings expectations and pricing resilience from major firms including PZ (+21.74%), NASCON (+18.65%), and Vitafoam (+17.79%), while the Insurance Index (+3.37%) gained on the back of renewed interest in NEM (+19.64%) and

Mansard (+7.71%).

In contrast, the Banking Index (-3.15%) was the only major laggard, reflecting profit-taking and capital reallocation rather than a fundamental sectoral decline. Following less impressive Q3 earnings, institutional investors strategically reduced exposure to Tier-1 banks such as Zenith Bank (-8.70%), GTCO (-4.69%), and Access Holdings (-4.68%) amid uncertainty surrounding regulatory capital recapitalization and liquidity demands. This selective sell-off underscores a deliberate shift in investor positioning, monetizing gains in liquid banking stocks to fund high-conviction moves into industrial and commodity-linked equities.

NGX Sectoral Returns in October

Sustained Bull Momentum and Strategic Capital Rotation

The list of the worst-performing stocks was dominated by small-to-mid cap equities that were acutely sensitive to weak corporate earnings, liquidity risk, and sector-specific challenges. The massive sectoral appreciation in Industrial Goods and Oil & Gas necessitates that the underlying bellwether stocks in these sectors deliver exceptional returns.

Outlook

In November, market activity is expected to be guided by an interplay of supportive corporate fundamentals and near-term risk triggers. On the upside, the release of 9M:2025 earnings across sectors is expected to drive further repricing of strong-performing stocks. A supportive macroeconomic environment, marked by easing inflation, stable interest rates, and rising oil prices, should help sustain valuations. Institutional investors are likely to maintain interest in fundamentally strong, high-quality stocks as a haven amid global uncertainty.

Sectoral momentum remains skewed toward industrials, oil & gas and consumer goods, while banking may continue to underperform amid regulatory and capital pressures. Investors should monitor key triggers, upcoming earnings prints, inflation and rate surprises, FX/naira developments, and policy-tax changes, which could either reinforce the bullish trend or prompt liquidity tightening.

However, the risk of profit-taking remains elevated: stocks that have delivered outsized gains may experience fund outflows, and uncertainties around the proposed Capital Gains Tax (CGT) could lead foreign and institutional investors to take pre-emptive positions out of the market.

FIXED INCOME

Disinflation and FX Stability Strengthen Market Confidence

October 2025 witnessed notable developments in the Nigerian fixed income market, shaped by dynamic liquidity conditions, active central bank interventions, and strong investor participation in both Treasury

Bills (NTBs) and Federal Government of Nigeria (FGN) Bond auctions. System liquidity experienced significant fluctuations, prompting continued monitoring and management by the Central Bank of Nigeria

(CBN) to maintain the restrictive monetary policy stance set by the 27.00% Monetary Policy Rate (MPR).

Investor appetite remained robust across primary auctions, particularly for longer-dated FGN Bonds, while secondary market activity reflected strategic positioning ahead of primary market events. Yield curve dynamics revealed an inversion in the nominal term structure, signaling market expectations of future monetary easing.

Domestic Money Market and System Liquidity

In October 2025, the Nigerian money market experienced significant liquidity fluctuations. Market liquidity started the month at ₦7.11 trillion on October 2, declined to ₦3.79 trillion by October 8, and later adjusted to ₦2.2 trillion on October 14 following Open Market Operation maturities. Despite these swings, the Central Bank of Nigeria (CBN) maintained a restrictive monetary stance, ensuring that the system

remained tightly controlled and that temporary liquidity surges did not spill over into unintended monetary easing or foreign exchange volatility.

The CBN successfully anchored short-term interest rates throughout the month. The benchmark Open Buy Back (OBB) rate remained at 24.50%, while the Overnight (O/N) rate was tightly managed between 24.87% and 24.88%. These actions demonstrate the effectiveness of the CBN’s sterilization operations in absorbing excess liquidity and preserving the policy objectives set by the 27.00% Monetary Policy Rate.

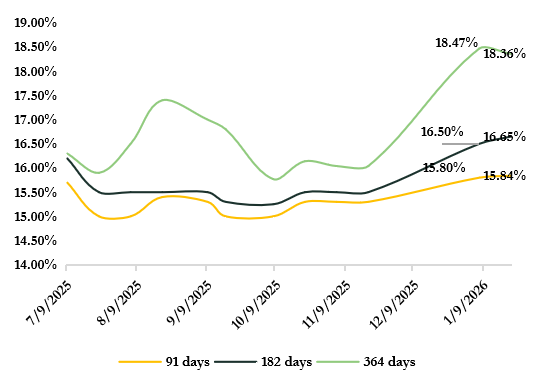

Investor demand for Treasury Bills remained robust, highlighting strong confidence in risk-free government instruments. The October 8 NTB auction, offering ₦570 billion, was oversubscribed with ₦1.06 trillion in bids, while the October 22 auction saw ₦650 billion offered across three tenors and total bids of ₦750.91 billion. The 364-day bill cleared at a stop

rate of 16.14%, yielding 19.25%, above headline inflation but below the MPR, reflecting a deliberate strategy by the CBN to encourage banks to hold short-term government paper and limit speculative pressures in the broader market.

FGN Bond Market Review

The FGN Bond market drew significant attention, with the DMO offering ₦260 billion through the re-opening of the 5-year AUG 2030 and 7-year JUN 2032 bonds. Investor participation was exceptionally

strong, totaling ₦1.27 trillion, with demand heavily concentrated in the 7-year tenor, which was oversubscribed by more than eight times. This reflects market expectations for future capital appreciation and suggests that monetary tightening is approaching its peak.

Marginal rates were set at 15.8320% for the 5-year bond and 15.8500% for the 7-year bond. Compared with the 364-day NTB yield of 19.25%, this represents a pronounced nominal yield curve inversion of roughly 340 basis points, signaling anticipation of future monetary easing. Investors increased duration exposure, favouring longer-term bonds over temporarily elevated short-term yields.

Secondary market activity mirrored these dynamics. Treasury bills began the month with bullish sentiment, slightly compressing yields to 16.50%, while FGN bonds traded mixed as participants repositioned ahead of the auction. Post-auction, mid-to-long-term yields declined sharply, supported by residual unmet demand from the 7-year tenor. The yield curve inversion created strategic choices: short-term NTBs provided high carry, while mid-to-long-dated FGN bonds offered capital preservation and potential price appreciation as the CBN gradually normalizes the curve.

Eurobonds and Global Confidence

Nigeria’s U.S. dollar–denominated sovereign bonds delivered a strong performance in October, reinforcing the narrative of improving global investor confidence, both in Nigeria’s credit trajectory and in the broader African Eurobond space.

Secondary market activity as of October 24, 2025, showed broad based tightening across the Nigerian Eurobond curve. The near-term 7.625% NOV 2025 bond traded at a yield of 4.337%, signaling very low perceived rollover or default risk, an outcome underpinned by improved liquidity conditions and effective debt management.

Long-dated bonds also recorded notable price appreciation. The 10.375% DEC 2034 bond traded at 112.020, well above par, reflecting substantial repricing of Nigeria’s sovereign risk. Investors have adjusted their assessment of the country’s creditworthiness materially lower, driving yields down relative to issuance levels. These gains align with a year marked by improving fiscal indicators, better FX liquidity, and stronger policy credibility.

FIXED INCOME

OUTLOOK

October 2025 served as a validation point for Nigeria’s macroeconomic reform trajectory, cementing a high degree of confidence among both domestic and international investors. The stabilization of the Naira, the successful disinflationary path, and the enhanced sovereign credit profile (marked by the FATF removal and successful Eurobond issuance) all contribute to a highly constructive outlook for Nigerian fixed income assets.