Accelerating Economic Development, the VC way

Venture capital (VC) has emerged as a catalyst in Nigeria’s journey toward sustainable economic growth and diversification. Traditionally reliant on oil and gas, the Nigerian economy is undergoing a paradigm shift toward innovation, entrepreneurship, and technology-driven solutions. VC is at the heart of this transformation, providing the critical financial resources, expertise, and strategic support that early-stage and high-growth startups require to thrive.

VC funding accelerates the development of sectors vital to Nigeria’s economic future, including financial technology (fintech), agriculture, clean energy, healthcare, and logistics. By backing entrepreneurs who address local challenges with scalable solutions, venture capital not only fosters the growth of individual businesses but also stimulates job creation, boosts productivity, and drives the adoption of new technologies across the broader economy.

By bridging the financing gap for startups and supporting Nigeria’s young and dynamic population, VC is catalysing a new generation of enterprises that are reshaping Africa’s economy. Its continued expansion is fundamental to unlocking Nigeria’s potential and achieving inclusive, technology-driven prosperity. Over the past decade, Nigeria has emerged as a pivotal hub for technology startups in Africa, driven by factors such as a burgeoning youth population, increasing internet penetration, and a growing appetite for digital solutions.

2024 VC Trends: Investment Climbs Globally, Contracts in Africa

According to the 2024 AVCA report, global venture capital investment reached US$313.6 bn, marking a 10% increase from the US$285.2 bn recorded in 2023. This figure accounts solely for VC deal volume and value, with deal values including Mezzanine and debt when the latter is part of a larger transaction that also involves equity. In contrast, Africa VC activity experienced a downturn in 2024, with US$2.6 bn invested across 427 deals, down from US$3.6 bn and 545 deals in 2023. This represents a 28% decline in value and a 22% drop in volume, highlighting a contraction in funding activity across the continent.

Despite this pullback, the 2024 figures suggest that Africa’s venture capital landscape may be approaching its peak. Notably, multi-region startups are shifting away from pan-African expansion strategies in favour of broader emerging market growth models. Leveraging later-stage capital, these startups are increasingly scaling into new geographies such as Southeast Asia, Latin America, and other developing regions, reflecting a strategic pivot toward global market diversification amid changing funding dynamics

The “Big Four” Dominate as FinTech Attracts the Lion’s Share of Funding

In 2024, West Africa maintained its lead in deal volume for the fourth consecutive year, driven primarily by Nigeria, which was the most active country by volume, accounting for 16% of deals. Despite lower volumes, multi-region deals garnered the highest total capital, while the ‘Big Four’ markets Nigeria, Egypt, Kenya, and South Africa continued to dominate, collectively accounting for 55% of total deal volume and 64% of capital deployed.

Despite a modest dip in total capital, the financial technology sector remains the star performer among African VC firms. In 2024, FinTech and Digital Banks led the market, accounting for 116 deals (34% of all tech-enabled rounds) and attracting US$1.4 billion in funding. This dynamic sector encompasses cryptocurrency platforms, embedded finance, and mobile wallets specifically designed for Africa’s largely unbanked population. Its continued dominance reflects both local demand and global trends, as digital banking solutions reshape access to financial services worldwide.

In 2024, African digital banks not only demonstrated strong regional appeal but also established a strong presence on the global stage. Tyme Bank’s US$250 million Series D ranked as the third-largest digital banking investment worldwide, while Moniepoint’s US$110 million Series C was the sixth-largest. An ongoing focus on Financials drove this momentum: 44% of deals originated in the sector, capturing half of the region’s total capital, trailed by the Information Technology (14%) and Consumer Staples (11%) sectors. The e-commerce and health care sectors witness declines in 2024, largely driven by a challenging operational environment, specifically, barriers to cost-effective growth and customer acquisition

The Nigerian Tech Startups 2024 Trend

Shifting focus to Nigeria, startups in the country secured approximately $410 million in funding in 2024, according to data from ‘Africa: The Big Deal.’ This figure remains the same as 2023, indicating a relatively stable funding environment despite broader market headwinds.

Notably, two major transactions, Moove’s $110 million raise and Moniepoint’s $110 million Series C round, accounted for over half of the total capital raised, underscoring the continued investor confidence in high-growth, later-stage Nigerian startups.

In Nigeria, the venture capital market is experiencing a shift towards funding startups that integrate sustainability and social impact into their business models. This shift is largely driven by a younger generation that values ethical practices and demands transparency from companies.

The following is a summary of the top venture capital deals in Nigeria in 2024.

| S/N | Startup | Sector | Amount Raised | Lead Investors |

|---|---|---|---|---|

|

1 |

Moove |

Mobility tech |

$110M |

Mubadala, The Latest Ventures, AfricInvest, Palm Drive Capital, Triatlum Advisors, and Future Africa |

|

2 |

Moniepoint |

Fin tech |

$110M |

Development Partners International (DPI), Google’s Africa Investment Fund, Verod Capital, and Lightrock. |

|

3 |

Yellow Card |

Blockchain |

$33M |

Blockchain Capital, Coinbase, Kraken, OpenSea and Worldcoin. |

|

4 |

Konexa |

Renewable Electricity |

$18M |

Climate Fund Managers (CFM) and Microsoft’s Climate Innovation Fund |

|

5 |

Tomato Jos |

Agri Business |

$12.2M |

N/A |

BRB’s Perspective: Our take on Venture Capital

At BRB Capital, we understand that the entrepreneurial journey is fraught with challenges, from securing early-stage funding to scaling a fast-growing enterprise. As a growing Nigerian investment firm with a global presence perspective, we see venture capital (VC) as a powerful instrument for fueling innovation, stimulating economic growth, and supporting visionary founders. We have financed high-potential startups and growth-stage businesses, enabling them to thrive in Nigeria’s dynamic marketplace and beyond.

BRB’s Approach to Venture Capital

A. Sector Focus

At BRB Capital, we prioritise sectors where we see the most potential for disruption and sustainable impact in Nigeria and the broader African context. These include

| SECTOR | SUBSECTOR AND FOCUS |

|---|---|

|

Technology and Innovation |

fintech, e-commerce, software-as-a-service, healthtech, edtech, regtech, insuretech, paytech |

|

Agribusiness and Food |

sustainable agriculture, food processing, logistics, sustainable land use, circular economy |

|

Energy and Infrastructure |

Renewable power solutions, energy efficiency, smart grids |

|

Consumer Goods and Services |

FMCG, retail, lifestyle brands |

B. Staged Investments

We support businesses at various stages of growth, whether you are an early-stage startup looking for seed funding or a growth-stage enterprise seeking Series A or beyond. Our staged approach allows us to partner with entrepreneurs at various stages of their journey, helping them secure the necessary capital to innovate, refine their business models, and penetrate new markets.

C. Hands-on Advisory

Funding alone is seldom enough to ensure success. Our team of industry specialists and operational experts complements funding by collaborating with portfolio companies to provide strategic guidance, market intelligence, and mentorship. We help founders navigate challenges such as product development, market entry, regulatory compliance, team building, and governance.

D. Responsible Investment

At BRB Capital, we prioritise responsible investing. We believe in supporting companies that create positive social, economic, and environmental outcomes. By adhering to robust Environmental, Social, and Governance (ESG) principles, we strive to ensure that our investments are inclusive and purpose-driven.

Conclusion?

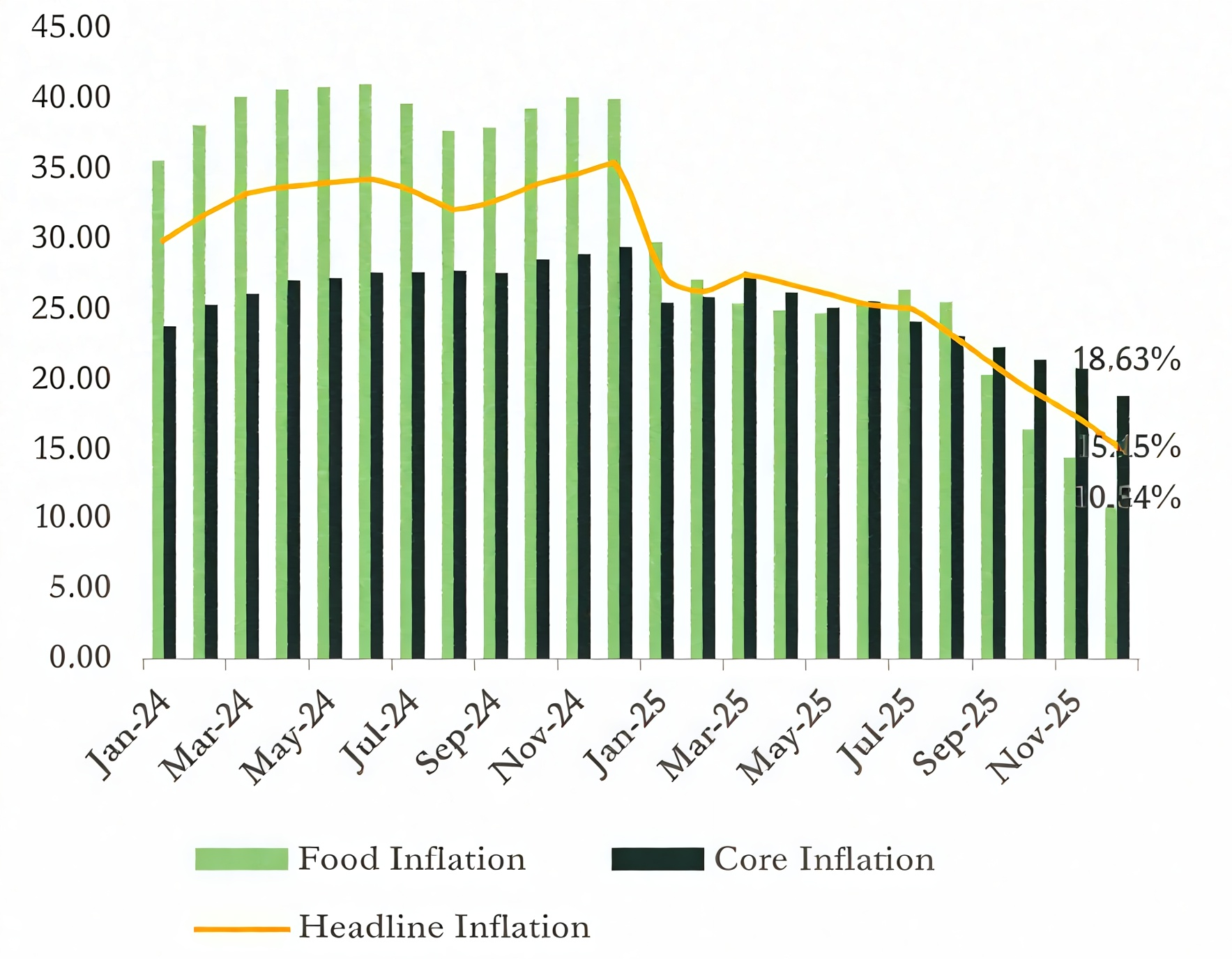

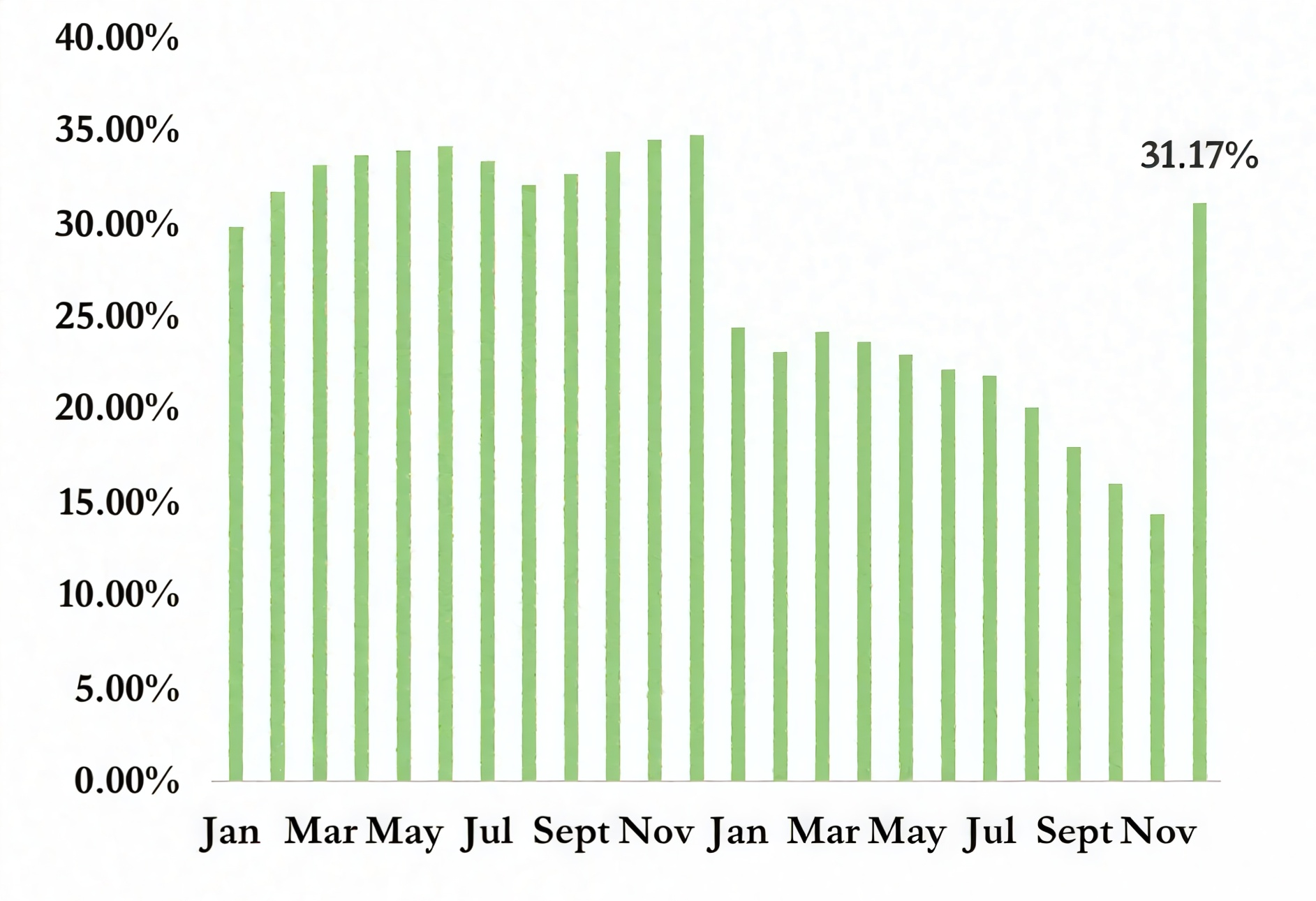

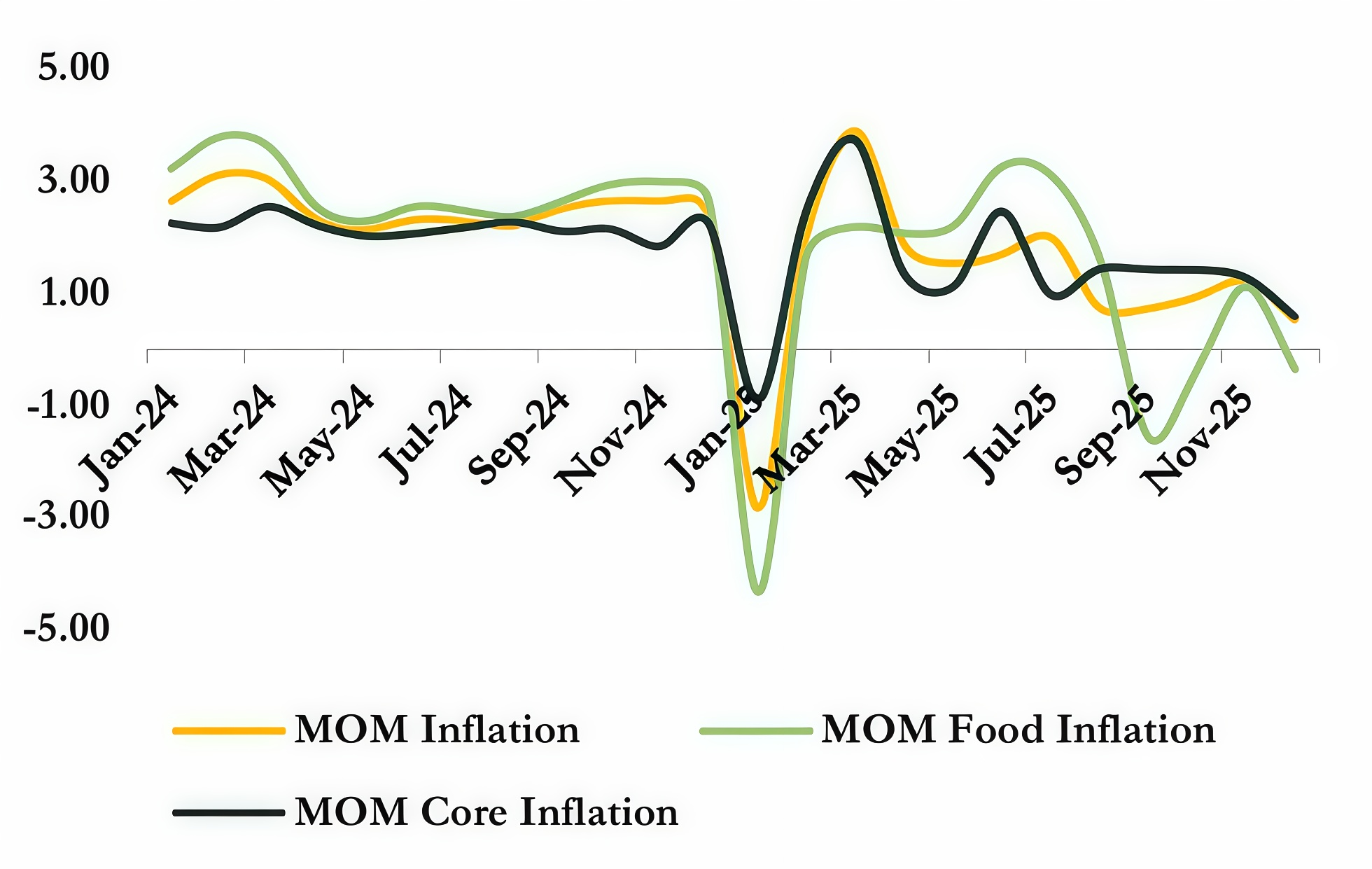

In conclusion, Nigeria’s venture capital ecosystem remains a cornerstone of innovation and economic diversification in Africa, despite the challenges posed by currency volatility, regulatory uncertainties, and infrastructure gaps. The persistent investor interest, especially in fintech, clean energy, and B2B commerce sectors, highlights the country’s vast potential to foster scalable, impact-driven startups that address real economic and social needs. With emerging policy reforms and growing collaboration between local and international investors, the Nigerian VC market is poised for resilient growth and continued leadership in the continent’s entrepreneurial landscape.

Looking ahead, sustaining this momentum requires fostering operational efficiency, enhancing regulatory clarity, and expanding infrastructure to unlock the full potential of Nigeria’s young, tech-savvy population. Venture capital will remain a critical enabler for innovative solutions that drive job creation, financial inclusion, and sustainable development. As Nigerian startups increasingly navigate global markets and adopt pragmatic growth models, the ecosystem is well-positioned to deliver significant economic value and cement Nigeria’s status as Africa’s foremost hub for venture investment.

Thanks for sharing

Keep it up lads

Okay nice

Good one bruh

Hi..please reach out

Nice post. Wanna see more of this.